20121112-Selected-Quantitative-Problems-Solutions1

Chapter 14 - Selected Quantitative Problems & Solutions

Quantitative Problems

Question 1(Useful)

The balance sheet of TriBank starts with an allowance for loan losses of $1.33 million.

During

the year, TriBank charges off worthless loans of $0.84 million, recovers $0.22 million on loans previously charged off, and charges current income for $1.48 million provisions for loan losses. Calculate the end of year allowance for loan losses.

Solution:1.33 M - 0.84 M + 0.22 M + 1.48 M = $2.19 M

Question 2(Useful)

X-Bank reported an ROE of 15% and an ROA of 1%. How well capitalized in this bank?

Solution:ROE = ROA ?EM

0.15 = 0.01 ?EM

EM= 15 = assets/equity

So equity/assets = 6.66%. This is a well-capitalized bank.

Question 3

In mid-1978, Wiggley S&L issued a standard 30-year fixed rate mortgage at 7.8% for $150,000.

36 months later, mortgage rates jumped to 13%. If the S&L sells the mortgage, how

much of a

loss is expected?

Solution:When issued, the required payment is:

PV= $150,000, I= 7.8/12, N= 360, FV= 0

Compute PMT.

PMT= $1,079.81

After 36 months, the mortgage balance is:

PMT= $1,079.81, I= 7.8/12, N= 324, FV= 0

Compute PV. PV= $145,764.43

However, at current rates, the remaining cash flows are worth:

PMT= $1,079.81, I = 13/12, N= 324, FV= 0

Compute PV. PV= $96,637.64

Wiggley S&L expects to take a loss of $49,126 if it sells the mortgage. Question 4

Refer to the previous question. In 1981 Congress allowed S&Ls to sell mortgages at a loss and to amortize the loss over the remaining life of the mortgage. If this were used for the previous question, how would the transaction have been recorded? What would be the annual adjustment? When would that end?

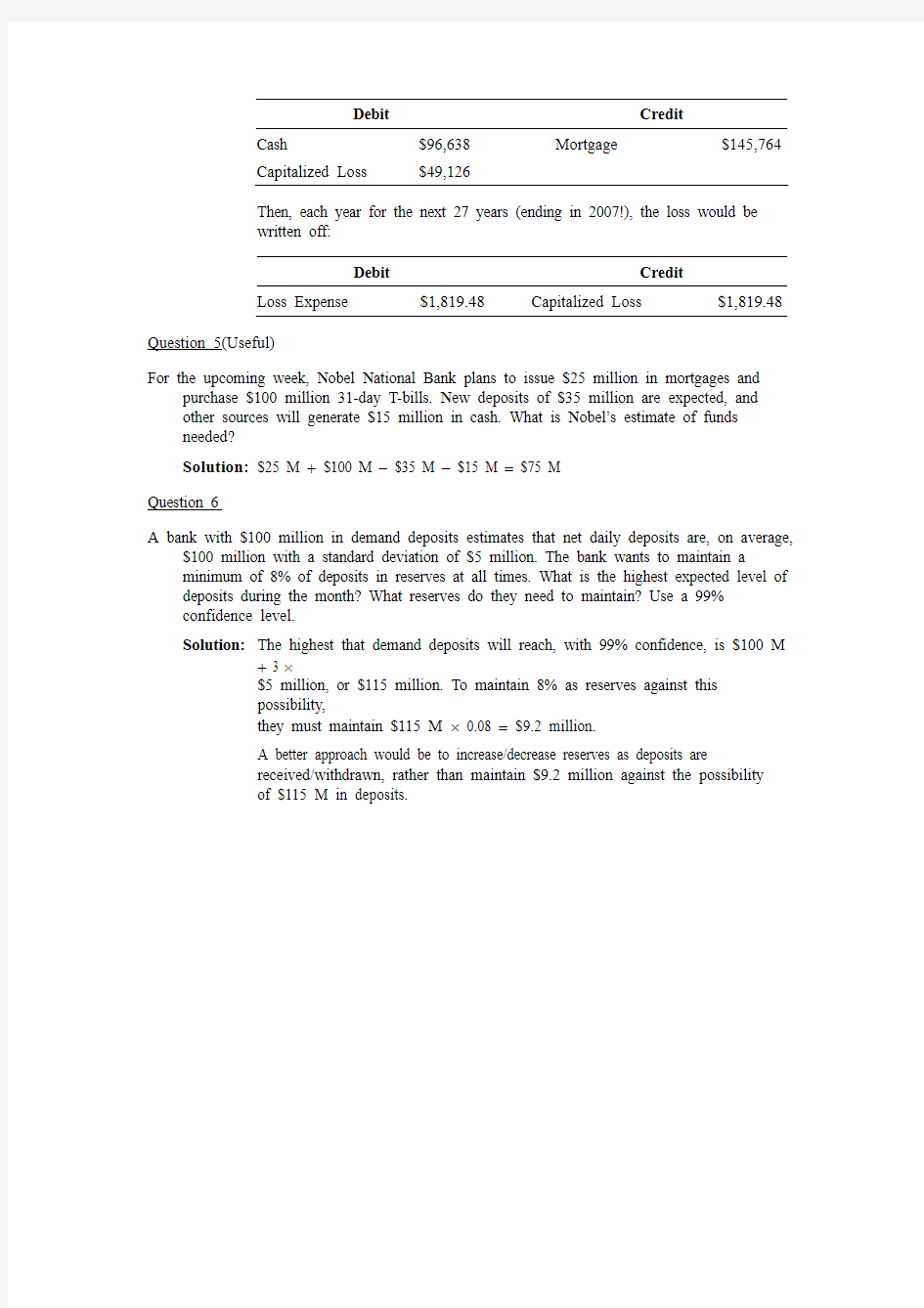

Solution: The sale would be recorded as:

Debit Credit

Cash $96,638 Mortgage $145,764

Capitalized Loss $49,126

Then, each year for the next 27 years (ending in 2007!), the loss would be

written off:

Debit Credit

Loss Expense $1,819.48 Capitalized Loss $1,819.48 Question 5(Useful)

For the upcoming week, Nobel National Bank plans to issue $25 million in mortgages and purchase $100 million 31-day T-bills. New deposits of $35 million are expected, and

other sources will generate $15 million in cash. What is Nobel’s estimate of funds

needed?

Solution:$25 M + $100 M - $35 M - $15 M = $75 M

Question 6

A bank with $100 million in demand deposits estimates that net daily deposits are, on average,

$100 million with a standard deviation of $5 million. The bank wants to maintain a

minimum of 8% of deposits in reserves at all times. What is the highest expected level of deposits during the month? What reserves do they need to maintain? Use a 99%

confidence level.

Solution:The highest that demand deposits will reach, with 99% confidence, is $100 M + 3 ?

$5 million, or $115 million. To maintain 8% as reserves against this

possibility,

they must maintain $115 M ? 0.08 = $9.2 million.

A better approach would be to increase/decrease reserves as deposits are

received/withdrawn, rather than maintain $9.2 million against the possibility

of $115 M in deposits.