香港会计报表--中英文对比

香港会计报表

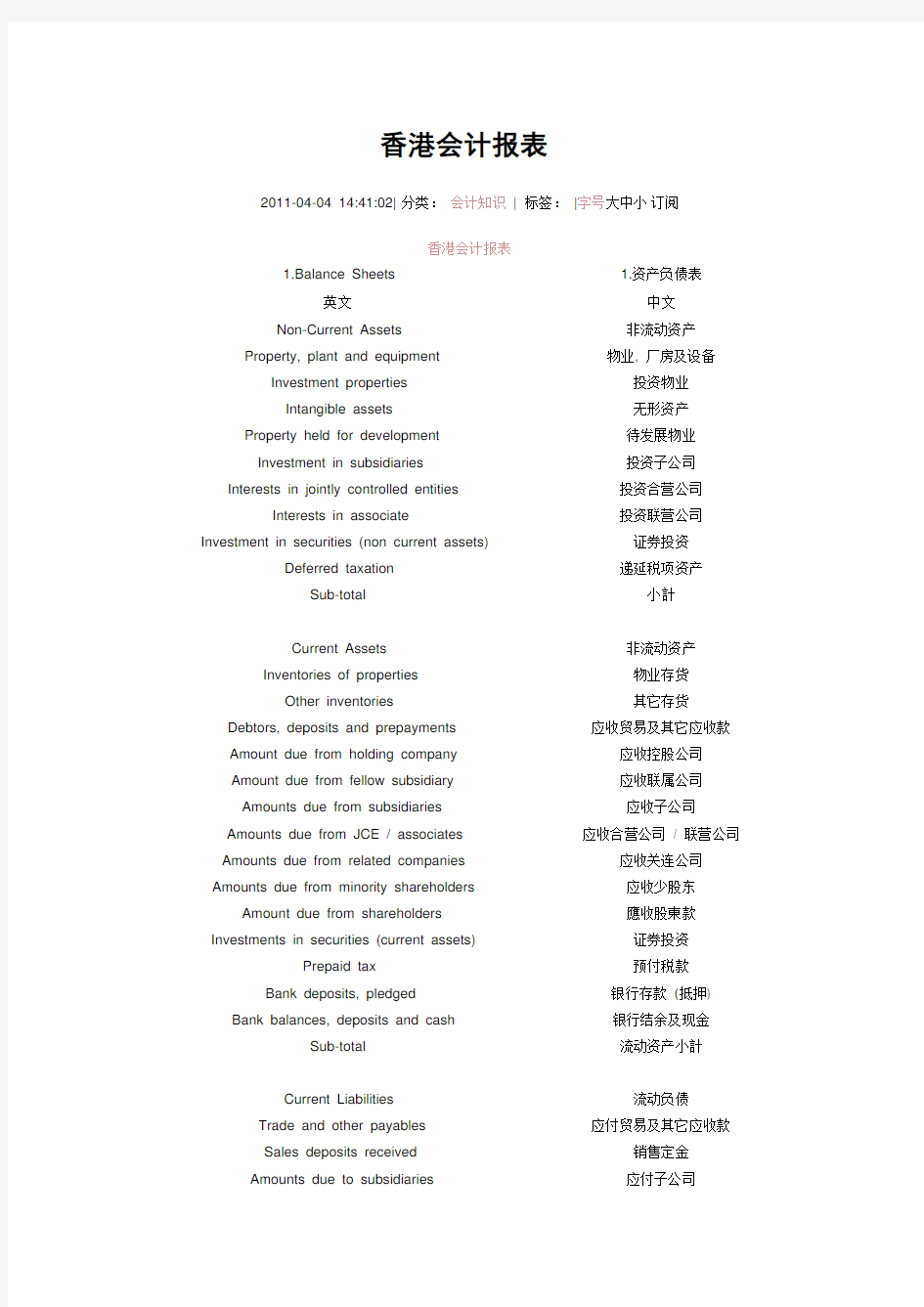

2011-04-04 14:41:02| 分类:会计知识| 标签:|字号大中小订阅

香港会计报表

1.Balance Sheets 1.资产负债表

英文中文

Non-Current Assets 非流动资产Property, plant and equipment 物业, 厂房及设备Investment properties 投资物业

Intangible assets 无形资产Property held for development 待发展物业

Investment in subsidiaries 投资子公司Interests in jointly controlled entities 投资合营公司Interests in associate 投资联营公司Investment in securities (non current assets) 证券投资Deferred taxation 递延税项资产

Sub-total 小計

Current Assets 非流动资产Inventories of properties 物业存货

Other inventories 其它存货Debtors, deposits and prepayments 应收贸易及其它应收款Amount due from holding company 应收控股公司

Amount due from fellow subsidiary 应收联属公司

Amounts due from subsidiaries 应收子公司Amounts due from JCE / associates 应收合营公司/ 联营公司Amounts due from related companies 应收关连公司Amounts due from minority shareholders 应收少股东Amount due from shareholders 應收股東款Investments in securities (current assets) 证券投资

Prepaid tax 预付税款Bank deposits, pledged 银行存款(抵押) Bank balances, deposits and cash 银行结余及现金

Sub-total 流动资产小計

Current Liabilities 流动负债Trade and other payables 应付贸易及其它应收款

Sales deposits received 销售定金

Amounts due to subsidiaries 应付子公司

Amounts due to immediate holding 应付控股公司Amounts due to fellow subsidiaries 应付联属公司

Amount due to JCE/associates 应付合营公司/ 联营公司Amounts due to related companies 应付关连公司Amount due to shareholders 应付股东款Amount due to minority shareholders 应付少股东

Bank borrowings, due within one year 银行借款(一年内) Other borrowings, due within one year 其它借款(一年内) Income tax payable 应付所得税

Sub-total 小計

Capital and Reserves 资本及储备Paid-up capital 资本Retained earnings b/f 年初未分配利润This year's profit 本年度纯利

Dividend 股息Reserve appropriation 利润分配-提取储备基金Statutory reserve 法定储备

Capital reserves 资本公积-股权投资准备Property revaluation reserve 投资物业重估储备Sub-total 所有者权益小計

Minority interests 少股东权益

Non-Current Liabilities 非流动负债

Bank borrowings, due after one year 银行借款(一年以上) Other borrowings, due after one year 其它借款(一年以上) Long term payables 长期应付款

Deferred taxation 递延税款

Sub-total 小計

2.INCOME STATEMENT 2.损益表

英文中文

Turnover 营业收入

Business Tax 主营业务税金及附加

Cost of sales 营业成本

经营毛利Gross Margin

Other operating income 其它业务收入Interest Income 利息收入

Gain from investment in securites 投资收益

Change in fair value of investment properties 投资物业公平价值之溢利Other operating expenses 其它业务支出

Selling expenses 营业费用

Administrative expenses 管理费用Provision on investment in securities 持有作买卖之投资公平价值之溢利Finance costs 财务费用Share of results of jointly controlled entities 应占合营公司业绩

Taxation 税项

Minority interests 少股东损益

This year's (profit) loss 本年度利纯

3.CASH-FLOWSTATEMENT 3.现金流量表

英文中文

Operating activities: 经营活动

Profit before tax 稅前經營溢利

Adjustment:- 調整:- Share of result of jointly controlled entities 应占共同控制公司业绩

Depreciation 折舊

Allowance for doubtful debts (补贴拨回),呆坏帐补贴Change in fair value of investment properties 投资物业公平价值之溢利Change in fair value of investments held for trading 持有作买卖之投资之公平价值溢利interest received 利息收入

Finance costs 财务费用Impairment loss on goodwill of JCE 共同控制公司之商誉减值损失Impairment loss on goodwill arising on acquisition of 增持予附属公司之权益导致商誉减值损失additional interest in subsidiaries 出售物业、厂房及设备之亏损(收益)Loss on disposal of PPE 持有作买卖之投资之亏损(收益)Gain on disposal of jointly controlled entities 出售一间共同控制公司之收益Write-back of trade payables 应付贸易账款拨回

未計流動資金變動前之經營業務及現金流

量

Increase in inventories of properties 物业存货之减少(增加)Increase in other inventories 其它存货之减少(增加)Increase in trade and other receivables 应收贸易及其它款项之增加

Increase in investments held for trading 持有作买卖之投资的减少(增加)

Increase in trade and other payables 应付贸易及其它账款之增加(减少)

Increase in sales deposits received 销售定金之增加(减少)

Cash generated from operation 經營業務產生之現金

Dividend received 已收股息

Tax paid- income tax 已付所得稅Tax paid- land value added tax 已付土地增值稅

Refund of tax 所得稅退回

Net cash inflow generated from operation 經營業務之現金流量淨額

投资业务

Interest received 利息收入Purchase of property, plant and equipment 购置物业,厂房及设备Proceeds from disposal of property, plant and equipment 出售物业,厂房及设备之收入

附属公司收购[size=+0] Acquisition of additional interest in sub 增持予附属公司之权益

Net cash from disposal of a subsidiary 出售一间附属公司之净现金收入

[size=+0]

Cash received on disposal of a JCE 出售一间共同控制公司之实收现金Dividend received from a JCE 收到一间共同控制公司的股息Repayment from related companies 来自关联公司的(预付款)还款Advances to JCE 向共同控制公司支付的预付款Capital contributions to JCE 向共同控制公司出资Net cash from investing activities 源自投资之现金净值

Financing activities 融資業務Capital contribution from minority shareholders 小股东投入资本

Decrease in amounts due to related companies 应付关联公司款额之减少Increase in amounts due to shareholders 应付股东款项之增加Increase in amounts due to JCE 应付共同控制公司款项之增加(减少)New bank loans raised 新筹集银行贷款

Repayment of bank loans 偿还银行贷款Repayment of other borrowings 偿还其它借款

Interest paid 已付股息

Dividend paid 已付利息

Net cash from financing activities 融資業務小计

Net increase/ (decrease) in cash & cash equivalent 現金及等同現金項目之變動

Net increase/ (decrease) in cash & cash equivalents 現金及等同現金項目之變動Cash & cash equivalent at 1 January 現金及等同現金項目承上年度

Cash & cash equivalent at 30 November 結轉現金及等同現金項目Analysis of the balance of cash and cash equivalents 現金及等同現金項目的分析

Bank balances and cash 銀行結存及現金

https://www.sodocs.net/doc/689328620.html,/sycc1/kjcs/200804/58.html

会计科目中英对照表

1001 现金Cash on hand

1002 银行存款Cash in bank

1009 其他货币资金Other monetary fund

100901 外埠存款Deposit in other cities

100902 银行本票Cashier's cheque

100903 银行汇票Bank draft

100904 信用卡Credit card

100905 信用保证金Deposit to creditor

100906 存出投资款Cash in investing account

1101 短期投资Short-term investments

110101 股票Short-term stock investments 110102 债券Short-term bond investments 110203 基金Short-term fund investments 110110 其他Other short-term investments

1102 短期投资跌价准

备

Provision for loss on decline in value of short-term investments

1111 应收票据Notes receivable

1121 应收股利Dividends receivable

1131 应收账款Accounts receivable

1133 其他应收款Other receivable

1141 坏账准备Provision for bad debts

1151 预付账款Advance to suppliers

1161 应收补贴款Subsidy receivable

1201 物资采购Materials purchased

1211 原材料Raw materials

1221 包装物Containers

1231 低值易耗品Low cost and short lived articles

1232 材料成本差异Cost variances of material

1241 自制半成品Semi-finished products

1243 库存商品Merchandise inventory

1244 商品进销差价Margin between selling and purchasing price on merchandise 1251 委托加工物资Material on consignment for further processing

1261 委托代销商品Goods on consignment- out

1271 受托代销商品Goods on consignment-in

1281 存货跌价准备Provision for impairment of inventories

1291 分期收款发出商

品

Goods on installment sales

1301 待摊费用Prepaid expense

1401 长期股权投资Long-term equity investments 140101 股票投资Long-term stock investments 140102 其他股权投资Other long-term equity investments 1402 长期债权投资Long-term debt investments 140201 债券投资Long-term bond investments 140202 其他债权投资Other long-term debt investments

1421 长期投资减值准

备

Provision for impairment of long-term investments

1431 委托贷款Entrusted loan

143101 本金Principal of entrusted loan 143102 利息Interest of entrusted loan 143103 减值准备Provision for impairment of entrusted loan 1501 固定资产Fixed assets-cost

1502 累计折旧Accumulated depreciation

1505 固定资产减值准

备

Provision for impairment of fixed assets

1601 工程物资Construction material 160101 专用材料Specific purpose materials 160102 专用设备Specific purpose equipments 160103 预付大型设备款Prepayments for major equipments

160104 为生产准备的工

具及器具

Tools and instruments prepared for production

1603 在建工程Construction in process

1605 在建工程减值准

备

Provision for impairment of construction in process

1701 固定资产清理Disposal of fixed assets

1801 无形资产Intangible assets

1815 未确认融资费用Unrecognized financing charges 1901 长期待摊费用Long-term deferred expenses 1911 待处理财产损溢Profit & loss of assets pending disposal

191101 待处理流动资产

损溢

Profit & loss of current-assets pending disposal

191102 待处理固定资产

损溢

Profit & loss of fixed assets pending disposal

2101 短期借款Short-term loans

2111 应付票据Notes payable

2121 应付账款Accounts payable 2131 预收账款Advance from customers 2141 代销商品款Accounts of consigned goods 2151 应付工资Wages payable

2153 应付福利费Welfare payable 2161 应付股利Dividends payable 2171 应交税金Taxes payable 217101 应交增值税Value added tax payable 21710101 进项税额Input VAT 21710102 已交税金Payment of VAT 21710103 转出未交增值税Outgoing of unpaid VAT 21710104 减免税款VAT relief 21710105 销项税额Output VAT 21710106 出口退税Refund of VAT for export 21710107 进项税额转出Outgoing of input VAT

21710108 出口抵减内销产

品应纳税额

Merchandise VAT from expert to domestic sale

21710109 转出多交增值税Outgoing of over-paid VAT 217102 未交增值税Unpaid VAT

217103 应交营业税Business tax payable 217104 应交消费税Consumer tax payable 217105 应交资源税Tax on natural resources payable 217106 应交所得税Income tax payable 217107 应交土地增值税Land appreciation tax payable

217108 应交城市维护建

设税

Urban maintenance and construction tax payable

217109 应交房产税Real estate tax payable 217110 应交土地使用税Land use tax payable 217111 应交车船使用税Vehicle and vessel usage tax payable 217112 应交个人所得税Personal income tax payable 2176 其他应交款Other fund payable

2181 其他应付款Other payables

2191 预提费用Accrued expenses

2201 待转资产价值Pending transfer value of assets 2211 预计负债Estimable liabilities

2301 长期借款Long-term loans

2311 应付债券Bonds payable

231101 债券面值Par value of bond

231102 债券溢价Bond premium

231103 债券折价Bond discount

231104 应计利息Accrued bond interest

2321 长期应付款Long-term payable

2331 专项应付款Specific account payable

2341 递延税款Deferred tax

3101 实收资本(或股

本)

Paid-in capital(or share capital)

3103 已归还投资Retired capital 3111 资本公积Capital reserve

311101 资本(或股本)溢

价

Capital (or share capital) premium

311102 接受捐赠非现金

资产准备

Restricted capital reserve of non-cash assets donation received

311103 接受现金捐赠Reserve of cash donation received 311104 股权投资准备Restricted capital reserve of equity investments 311105 拨款转入Government grants received

311106 外币资本折算差

额

Foreign currency capital conversion difference

311107 其他资本公积Other capital reserve 3121 盈余公积Surplus reserve 312101 法定盈余公积Statutory surplus reserve 312102 任意盈余公积Discretionary earning surplus 312103 法定公益金Statutory public welfare fund 312104 储备基金Reserve fund 312105 企业发展基金Enterprise development fund 312106 利润归还投资Profit return for investment 3131 本年利润Profit & loss summary 3141 利润分配Distribution profit 314101 其他转入Other adjustments

314102 提取法定盈余公

积金

Extract for statutory surplus reserve

314103 提取法定公益金Extract for statutory public welfare fund 314104 提取储备基金Extract for reserve fund

314105 提取企业发展基

金

Extract for enterprise development fund

314106 提取职工奖励及

福利基金

Extract for staff bonus and welfare fund

314107 利润归还投资Profit return of capital invested 314108 应付优先股股利Preference share dividend payable

314109 提取任意盈余公

积

Extract for discretionary earning surplus

314110 应付普通股股利Ordinary share dividend payable

314111

转作资本(或股

本)的普通股股利

Ordinary share dividend transfer to capital (or share)

314115 未分配利润Undistributed profit 4101 生产成本Cost of production

410101 基本生产成本Basic production cost 410102 辅助生产成本Auxiliary production cost 4105 制造费用Manufacturing overheads 4107 劳务成本Labor cost

5101 主营业务收入Sales revenue

5102 其他业务收入Revenues from other operations 5201 投资收益Investment income

5203 补贴收入Subsidy income

5301 营业外收入Non-operating profit 5401 主营业务成本Cost of sales

5402 主营业务税金及

附加

Sales tax

5405 其他业务支出Cost of other operations

5501 营业费用Operating expenses

5502 管理费用General and administrative expenses 5503 财务费用Financial expenses

5601 营业外支出Non-operating expenses

5701 所得税Income tax

5801 以前年度损益调

整

Prior period profit & loss adjustment

高级财务会计—外币财务报表折算练习题(含答案)

高级财务会计:外币财务报表折算 练习题(含答案) 一、选择题 1.外币报表折算为人民币报表时,利润分配表中的“未分配利润”项目应当()。 A.根据折算后利润分配表中的其他项目的数额计算确定 B.按历史汇率折算 C.按现行汇率折算 D.按平均汇率折算 2. 按照《企业会计准则第19号——外币折算》,外币报表折算差额在会计报表中应作为()。 A.递延损益列示 B.管理费用列示 C.财务费用列示 D.外币报表折算差额单列 3.对外币会计报表折算后不改变资产和负债的内部结构和比例关系的折算方法是()。 A.时态法 B.现行汇率法 C.流动性与非流动性项目法 D.货币性与非货币性项目法 4.在采用货币与非货币项目法进行外币会计报表折算的情况下,按照历史汇率折算的项目是()。 A.应收账款项目 B.存货项目 C.未分配利润项目 D.长期负债项目 5.采用现行汇率法折算外币会计报表时,按照历史汇率折算的会计报表项目有()。 A.存货项目 B.短期投资项目 C.应付债券项目 D.实收资本项目 6.采用时态法折算外币会计报表时,按照历史汇率折算的会计报表项目有()。 A.应付账款项目 B.按成本计价的存货项目 C.按市价计价的投资项目 D.按成本计价的投资项目 7.外币报表折算可供选择的汇率主要有()三种。

A. 历史汇率 B. 现行汇率 C. 平均汇率 D.远期汇率 8.根据我国《企业会计准则第19号——外币折算》的规定,可以采用资产负债表日即期汇率折算的会计报表项目有()。 A.长期股权投资项目 B.未分配利润项目 C.无形资产项目 D.长期应付款项目 9.按照《企业会计准则第19号——外币折算》,外币会计报表中可以按照交易发生日即期汇率折算的项目有()。 A.营业成本 B.营业外支出 C.营业收入 D.管理费用 10.境外经营,是指企业在境外的()。 A.子公司 B.分支机构 C.联营企业 D.合营企业 二、业务题 1.某国外子公司的财务报表需折算为美元。有关资料如下: 汇率设定: 债券、股份发行日的汇率LC1.00=US$0.23 固定资产取得时日的汇率LC1.00=US$0.23 年初存货折算汇率LC1.00=US$0.19 年末存货折算汇率LC1.00=US$0.22 股利支付日的汇率LC1.00=US$0.21 20×6年度平均汇率LC1.00=US$0.20 20×5年12月31日汇率LC1.00=US$0.18 20×6年12月31日汇率LC1.00=US$0.24

财务报表中英文对照

财务报表中英文对照 1.资产负债表Balance Sheet 项目ITEM 货币资金Cash 短期投资Short term investments 应收票据Notes receivable 应收股利Dividend receivable 应收利息Interest receivable 应收帐款Accounts receivable 其他应收款Other receivables 预付帐款Accounts prepaid 期货保证金Future guarantee 应收补贴款Allowance receivable 应收出口退税Export drawback receivable 存货Inventories 其中:原材料Including:Raw materials 产成品(库存商品) Finished goods 待摊费用Prepaid and deferred expenses 待处理流动资产净损失Unsettled G/L on current assets 一年内到期的长期债权投资Long-term debenture investment falling due in a year 其他流动资产Other current assets 流动资产合计Total current assets 长期投资:Long-term investment: 其中:长期股权投资Including long term equity investment 长期债权投资Long term securities investment *合并价差Incorporating price difference 长期投资合计Total long-term investment 固定资产原价Fixed assets-cost 减:累计折旧Less:Accumulated Dpreciation 固定资产净值Fixed assets-net value 减:固定资产减值准备Less:Impairment of fixed assets 固定资产净额Net value of fixed assets 固定资产清理Disposal of fixed assets 工程物资Project material 在建工程Construction in Progress 待处理固定资产净损失Unsettled G/L on fixed assets 固定资产合计Total tangible assets 无形资产Intangible assets 其中:土地使用权Including and use rights 递延资产(长期待摊费用)Deferred assets

会计报表科目中英文对照

一、企业财务会计报表封面FINANCIAL REPORT COVER 报表所属期间之期末时间点Period Ended 所属月份Reporting Period 报出日期Submit Date 记账本位币币种Local Reporting Currency 审核人Verifier 填表人Preparer 二、资产负债表Balance Sheet 资产Assets 流动资产Current Assets 货币资金Bank and Cash 短期投资Current Investment 一年内到期委托贷款Entrusted loan receivable due within one year 减:一年内到期委托贷款减值准备Less: Impairment for Entrusted loan receivable due within one year 减:短期投资跌价准备Less: Impairment for current investment 短期投资净额Net bal of current investment 应收票据Notes receivable 应收股利Dividend receivable 应收利息Interest receivable 应收账款Account receivable 减:应收账款坏账准备Less: Bad debt provision for Account receivable 应收账款净额Net bal of Account receivable 其他应收款Other receivable 减:其他应收款坏账准备Less: Bad debt provision for Other receivable 其他应收款净额Net bal of Other receivable 预付账款Prepayment 应收补贴款Subsidy receivable 存货Inventory 减:存货跌价准备Less: Provision for Inventory 存货净额Net bal of Inventory 已完工尚未结算款Amount due from customer for contract work 待摊费用Deferred Expense 一年内到期的长期债权投资Long-term debt investment due within one year 一年内到期的应收融资租赁款Finance lease receivables due within one year 其他流动资产Other current assets 流动资产合计Total current assets 长期投资Long-term investment 长期股权投资Long-term equity investment 委托贷款Entrusted loan receivable 长期债权投资Long-term debt investment 长期投资合计Total for long-term investment

中英文对照版财务报表

一、企业财务会计报表封面 FINANCIAL REPORT COVER 报表所属期间之期末时间点 Period Ended 所属月份 Reporting Period 报出日期 Submit Date 记账本位币币种 Local Reporting Currency 审核人 Verifier 填表人 Preparer 二、资产负债表 Balance Sheet 资产 Assets 流动资产 Current Assets 货币资金 Bank and Cash 短期投资 Current Investment 一年内到期委托贷款 Entrusted loan receivable due within one year 减:一年内到期委托贷款减值准备 Less: Impairment for Entrusted loan receivable due within one year 减:短期投资跌价准备 Less: Impairment for current investment 短期投资净额 Net bal of current investment 应收票据 Notes receivable 应收股利 Dividend receivable 应收利息 Interest receivable 应收账款 Account receivable 减:应收账款坏账准备 Less: Bad debt provision for Account receivable 应收账款净额 Net bal of Account receivable 其他应收款 Other receivable 减:其他应收款坏账准备 Less: Bad debt provision for Other receivable 其他应收款净额 Net bal of Other receivable 预付账款 Prepayment 应收补贴款 Subsidy receivable 存货 Inventory 减:存货跌价准备 Less: Provision for Inventory 存货净额 Net bal of Inventory 已完工尚未结算款 Amount due from customer for contract work 待摊费用 Deferred Expense 一年内到期的长期债权投资 Long-term debt investment due within one year 一年内到期的应收融资租赁款 Finance lease receivables due within one year 其他流动资产 Other current assets 流动资产合计 Total current assets 长期投资 Long-term investment 长期股权投资 Long-term equity investment 委托贷款 Entrusted loan receivable 长期债权投资 Long-term debt investment

会计报表术语中英文对照

会计报表术语中英文对照 一、损益表INCOME STA TEMENT Aggregate income statement?合并损益表 Operating Results?经营业绩 FINANCIAL HIGHLIGHTS?财务摘要 Gross revenues?总收入/毛收入 Net revenues ?销售收入/净收入 Sales?销售额 Turnover?营业额 Cost of revenues ?销售成本 Gross profit ?毛利润 Gross margin?毛利率 Other income and gain?其他收入及利得 EBITDA?息、税、折旧、摊销前利润(EBITDA) EBITDA margin?EBITDA率 EBITA?息、税、摊销前利润 EBIT?息税前利润/营业利润 Operating income(loss)?营业利润/(亏损) Operating profit?营业利润 Operating margin?营业利润率 EBIT margin?EBIT率(营业利润率) Profit before disposal of investments?出售投资前利润 Operating expenses:?营业费用: Research and development costs (R&D)?研发费用 marketing expensesSelling expenses?销售费用 Cost of revenues?营业成本 Selling Cost?销售成本 Sales and marketing expenses Selling and marketing expenses?销售费用、或销售及市场推广费用 Selling and distribution costs?营销费用/行销费用 General and administrative expenses ?管理费用/一般及管理费用 Administrative expenses?管理费用 Operating income(loss)?营业利润/(亏损) Profit from operating activities?营业利润/经营活动之利润 Finance costs?财务费用/财务成本 Financial result?财务费用 Finance income?财务收益 Change in fair value of derivative liability associated with Series B convertible redeemable preference shares?可转换可赎回优先股B相关衍生负债公允值变动 Loss on the derivative component of convertible bonds?可换股债券衍生工具之损失 Equity loss of affiliates?子公司权益损失 Government grant income ?政府补助 Other (expense) / income ?其他收入/(费用) Loss before income taxes ?税前损失

会计报表中英文对照

?会计报表中英文对照

Accounting

1.Financial reporting(财务报告)includes not only financial statements but also other means of communicating information that relates,directly or indirectly,to the information provided by a business enterprise’s accounting system----that is,information about an enterprise’s resources,obligations, earnings,etc. 2.Objectives of financial reporting:财务报告的目标 Financial reporting should: (1)Provide information that helps in making investment and credit decisions. (2)Provide information that enables assessing future cash flows. (3)Provide information that enables users to learn about economic resources, claims against those resources,and changes in them. 3.Basic accounting assumptions基本会计假设 (1)Economic entity assumption会计主体假设 This assumption simply says that the business and the owner of the business are two separate legal and economic entities.Each entity should account and report its own financial activities. (2)Going concern assumption持续经营假设 This assumption states that the enterprise will continue in operation long enough to carry out its existing objectives. This assumption enables accountants to make estimates about asset lives and how transactions might be amortized over time. This assumption enables an accountant to use accrual accounting which records accrual and deferral entries as of each balance sheet date. (3)Time period assumption会计分期假设 This assumption assumes that the economic life of a business can be divided into artificial time periods. The most typical time segment=Calendar Year Next most typical time segment=Fiscal Year (4)Monetary unit assumption货币计量假设 This assumption states that only transaction data that can be expressed in terms of money be included in the accounting records,and the unit of measure remains relatively constant over time in terms of purchasing power. In essence,this assumption disregards the effects of inflation or deflation in the economy in which the entity operates. This assumption provides support for the"Historical Cost"principle. 4.Accrual-basis accounting权责发生制会计 5.Qualitative characteristics会计信息质量特征 (1)Reliability可靠性 For accounting information to be reliable,it must be dependable and trustworthy. Accounting information is reliable to the extend that it is: Verifiable:means that information has been objectively determined,arrived at, or created.More than one person could consider the facts of a situation and reach a similar conclusion.

外商投资企业会计报表项目中英文对照表

字体大小:大| 中| 小2006-12-14 16:46 - 阅读:36599 - 评论:0 外商投资企业会计报表项目中英文对照表(供参考) 外商投资工业企业会计报表 Financial Statements for Industrial Enterprises with Foreign Investment ━━━━━━━━━━━━━━━━ (企业名称NAME OF ENTERPRISE) 资产负债表BALANCE SHEET _____年_____月_____日会外工01表 As of (month/date)19 FORM AFI(INDUSTRIAL)-01 ) 单位MONETARY UNIT: }1 ━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━, 资产行次年初数期末数 ASSETS LINE NO. AT BEG.OF YEAR AT END OF PERIOD ──────────────────────────────────────── 流动资产:CURRENT ASSETS }现金Cash on hand 银行存款Cash in bank 有价证券Marketable securities 应收票据Notes receivable 应收账款Accounts receivable

减:坏账准备Less: provision for bad debts 预付货款Advances to suppliers 其他应收款Other receivables 待摊费用Prepaid expense 存货Inventories 减:存货变现损失准备Less: Provision for loss on realization of inventories 一年内到期的长期投资Long-term investments maturing within one year 其他流动资产Other current assets 流动资产合计Total current assets 长期投资:LONG-TERM INVESTMENTS 长期投资Long-term investments 一年以上的应收款项Receivables collectible after one year 固定资产:FIXED ASSETS: 固定资产原价Fixed assets-cost 21 减:累计折旧Less: Accumulated depreciation 固定资产净值Fixed assets-net value 23 固定资产清理Disposal of fixed assets 27 在建工程:CONSTRUCTION IN PROGRESS: 在建工程Construction in progress 无形资产:INTANGIBLE ASSETS: 场地使用权Land occupancy right 29 3)>工业产权及专有技术Industry property rights and proprietary )technology 30 其他无形资产Other intangible assets 无形资产合计Total intangible assets 其他资产:OTHER ASSETS: -开办费Organization expense

2017年萍乡市注册会计师会计会计外币财务报表折算练习题

2017年萍乡市注册会计师《会计》会计外币财务报表折算练习题 单项选择题 1、M公司的境外子公司编报报表的货币为美元。母公司本期期末汇率为1美元=6.60 元人民币,平均汇率为1美元=6.46元人民币,该企业利润表和所有者权益变动表采用平均汇率折算。资产负债表中“盈余公积”期初数为150万美元,折合人民币1 215万元,本期所有者权益变动表“提取盈余公积”为180万美元,则本期该企业资产负债表“盈余公积”的期末数额应该是人民币( )。 A、2377.8万元 B、346.5万元 C、147.9万元 D、1276.50万元 【答案】A 【解析】本题考查知识点:外币财务报表折算。本期该企业资产负债表“盈余公积”的期末数额=1 215+180×6.46=2 377.8(万元)。 2、2015年1月1日,甲公司董事会批准了管理层提出的客户忠诚度计划。该客户忠诚度计划为:持积分卡的客户在甲公司消费一定金额时,甲公司向其授予奖励积分,客户可以使用奖励积分(每一奖励积分的公允价值为0.01元)。2015年度,甲公司销售各类商品共计10 000万元(不包括客户使用奖励积分购买的商品),授予客户奖励积分共计10 000万分,客户使用奖励积分共计7 200万分。2×14年年末,甲公司估计2015年度授予的奖励积分将有90%使用。不考虑其他因素,甲公司2015年度应确认的收入总额为( )万元。 A.9 972 B.9 980 C.9 900 D.10 000 【答案】B 【解析】2015年度授予奖励积分的公允价值=10 000×0.01=100(万元),2015年度因销售商品应当确认的销售收入=10 000-100=9 900(万元);2015年度因客户使用奖励积分应当

(完整word版)会计报表中英文对照

会计报表中英文对照

Accounting

1. Financial reporting(财务报告) includes not only financial statements but also other means of communicating information that relates, directly or indirectly, to the information provided by a business enterprise’s accounting system----that is, information about an enterprise’s resources, obligations, earnings, etc. 2. Objectives of financial reporting: 财务报告的目标 Financial reporting should: (1) Provide information that helps in making investment and credit decisions. (2) Provide information that enables assessing future cash flows. (3) Provide information that enables users to learn about economic resources, claims against those resources, and changes in them. 3. Basic accounting assumptions 基本会计假设 (1) Economic entity assumption 会计主体假设 This assumption simply says that the business and the owner of the business are two separate legal and economic entities. Each entity should account and report its own financial activities. (2) Going concern assumption 持续经营假设 This assumption states that the enterprise will continue in operation long enough to carry out its existing objectives. This assumption enables accountants to make estimates about asset lives and how transactions might be amortized over time. This assumption enables an accountant to use accrual accounting which records accrual and deferral entries as of each balance sheet date. (3) Time period assumption 会计分期假设 This assumption assumes that the economic life of a business can be divided into artificial time periods. The most typical time segment = Calendar Year Next most typical time segment = Fiscal Year (4) Monetary unit assumption 货币计量假设 This assumption states that only transaction data that can be expressed in terms of money be included in the accounting records, and the unit of measure remains relatively constant over time in terms of purchasing power. In essence, this assumption disregards the effects of inflation or deflation in the economy in which the entity operates. This assumption provides support for the "Historical Cost" principle. 4. Accrual-basis accounting 权责发生制会计 5. Qualitative characteristics 会计信息质量特征 (1) Reliability 可靠性 For accounting information to be reliable, it must be dependable and trustworthy. Accounting information is reliable to the extend that it is: Verifiable: means that information has been objectively determined, arrived at, or created. More than one person could consider the facts of a situation and reach a similar conclusion. Representationally faithful: that something is what it is represented to be. For example, if a machine is listed as a fixed asset on the balance sheet, then the company

会计报表中英文对照

会计报表中英文对照?

Accounting 1. Financial reporting(财务报告) includes not only financial statements but also other means of communicating information that relates, directly or indirectly, to the information provided by a business enterprise's accounting system----that is, information about an enterprise's resources, obligations, earnings, etc. 2. Objectives of financial reporting: 财务报告目标 Financial reporting should:

(1) Provide information that helps in making investment and credit decisions. (2) Provide information that enables assessing future cash flows. (3) Provide information that enables users to learn about economic resources, claims against those resources, and changes in them. 3. Basic accounting assumptions 基本会计假设 (1) Economic entity assumption 会计主体假设 This assumption simply says that the business and the owner of the business are two separate legal and economic entities. Each entity should account and report its own financial activities. (2) Going concern assumption 持续经营假设 This assumption states that the enterprise will continue in operation long enough to carry out its existing objectives. This assumption enables accountants to make estimates about asset lives and how transactions might be amortized over time. This assumption enables an accountant to use accrual accounting which records accrual and deferral entries as of each balance sheet date. (3) Time period assumption 会计分期假设 This assumption assumes that the economic life of a business can be divided into artificial time periods. The most typical time segment = Calendar Year Next most typical time segment = Fiscal Year (4) Monetary unit assumption 货币计量假设 This assumption states that only transaction data that can be expressed in terms of money be included in the accounting records, and the unit of measure remains relatively constant over time in terms of purchasing power. In essence, this assumption disregards the effects of inflation or deflation in the economy in which the entity operates. This assumption provides support for the Historical Cost principle. 4. Accrual-basis accounting 权责发生制会计 5. Qualitative characteristics 会计信息质量特征 (1) Reliability 可靠性 For accounting information to be reliable, it must be dependable and trustworthy. Accounting information is reliable to the extend that it is: Verifiable: means that information has been objectively determined, arrived at, or created. More than one person could consider the facts of a situation and reach a similar conclusion. Representationally faithful: that something is what it is represented to be. For example, if a machine is listed as a fixed asset on the balance sheet, then the company can prove that the machine exists, is owned by the company, is in working condition, and is currently being used to support the revenue generating activities of the company. Neutral: means that information is presented in accordance with generally accepted accounting principles and practices, and without bias. (2) Relevance 相关性

会计报表附注中英文对照

最新会计报表附注中英文对照. 简式) 最新会计报表附注中英文对照(字号:1 2008-12-27 14:00:46 阅读2069 评论审计报告中英对照

大中小 **铸造有限公司 会计报表附注 2006年度 **foundry Co., Ltd. Notes to Financial Statements for the Year Ended December 31, 2006 一、公司概况 I. Profile of Company **铸造有限公司(以下简称“本公司”),成立于2005年12月14日,为有限责任公司。经营地址为**玛钢工业园区。企业法人营业执照注

册号为**,注册资本为人民币壹佰万元。经营范围:铸造、加工、销售;管道连接件、铝合金铸件、塑料制品;机加工、热镀各种铸件;经销各种炉料、生铁、机械设备;运输(国家有限制运输的除外)**foundry Co., Ltd. (hereinafter referred to as “the company”), a limited liability company with the registered capital of 1,000,000 RMB, was set up on Dec. 14, 2005. The company is located at ** industry zone. Its business license No. is **. The company is mainly engaged in foundry, processing, vendition, pipeline connector, Aluminum alloy casting, Plastic products,

三大会计报表中英文对照

资产负债表Balance Sheet 项目ITEM 货币资金Cash 短期投资Short term investments 应收票据Notes receivable 应收股利Dividend receivable 应收利息Interest receivable 应收帐款Accounts receivable 其他应收款Other receivables 预付帐款Accounts prepaid 期货保证金Future guarantee 应收补贴款Allowance receivable 应收出口退税Export drawback receivable 存货Inventories 其中:原材料Including:Raw materials 产成品(库存商品) Finished goods 待摊费用Prepaid and deferred expenses 待处理流动资产净损失Unsettled G/L on current assets 一年内到期的长期债权投资Long-term debenture investment falling due in a yaear 其他流动资产Other current assets 流动资产合计Total current assets 长期投资:Long-term investment: 其中:长期股权投资Including long term equity investment 长期债权投资Long term securities investment *合并价差Incorporating price difference 长期投资合计Total long-term investment 固定资产原价Fixed assets-cost 减:累计折旧Less:Accumulated Dpreciation 固定资产净值Fixed assets-net value 减:固定资产减值准备Less:Impairment of fixed assets 固定资产净额Net value of fixed assets 固定资产清理Disposal of fixed assets 工程物资Project material 在建工程Construction in Progress 待处理固定资产净损失Unsettled G/L on fixed assets 固定资产合计Total tangible assets 无形资产Intangible assets 其中:土地使用权Including and use rights 递延资产(长期待摊费用)Deferred assets 其中:固定资产修理Including:Fixed assets repair 固定资产改良支出Improvement expenditure of fixed assets 其他长期资产Other long term assets 其中:特准储备物资Among it:Specially approved reserving materials 无形及其他资产合计Total intangible assets and other assets