2012CPA会计英语第五单元(完整版)

Unit 5 Special Issues

Government grants

Definition

A government grant is defined as assistance, in the form of cash or other assets, given in return for compliance with certain conditions relating to the enterprise’s operations.

Accounting treatment

An entity should not recognize government grants ( including non-monetary grants at fair value) until it has reasonable assurance that :

?The entity will comply with any conditions attached to the grant

?The entity will actually receive the grant

IAS 20 requires grants to be recognized under the income approach (收益法), i.e. grants are recognized as income over the relevant periods to match them with related costs which they have been received to compensate. This should be done on a systematic basis of matching.

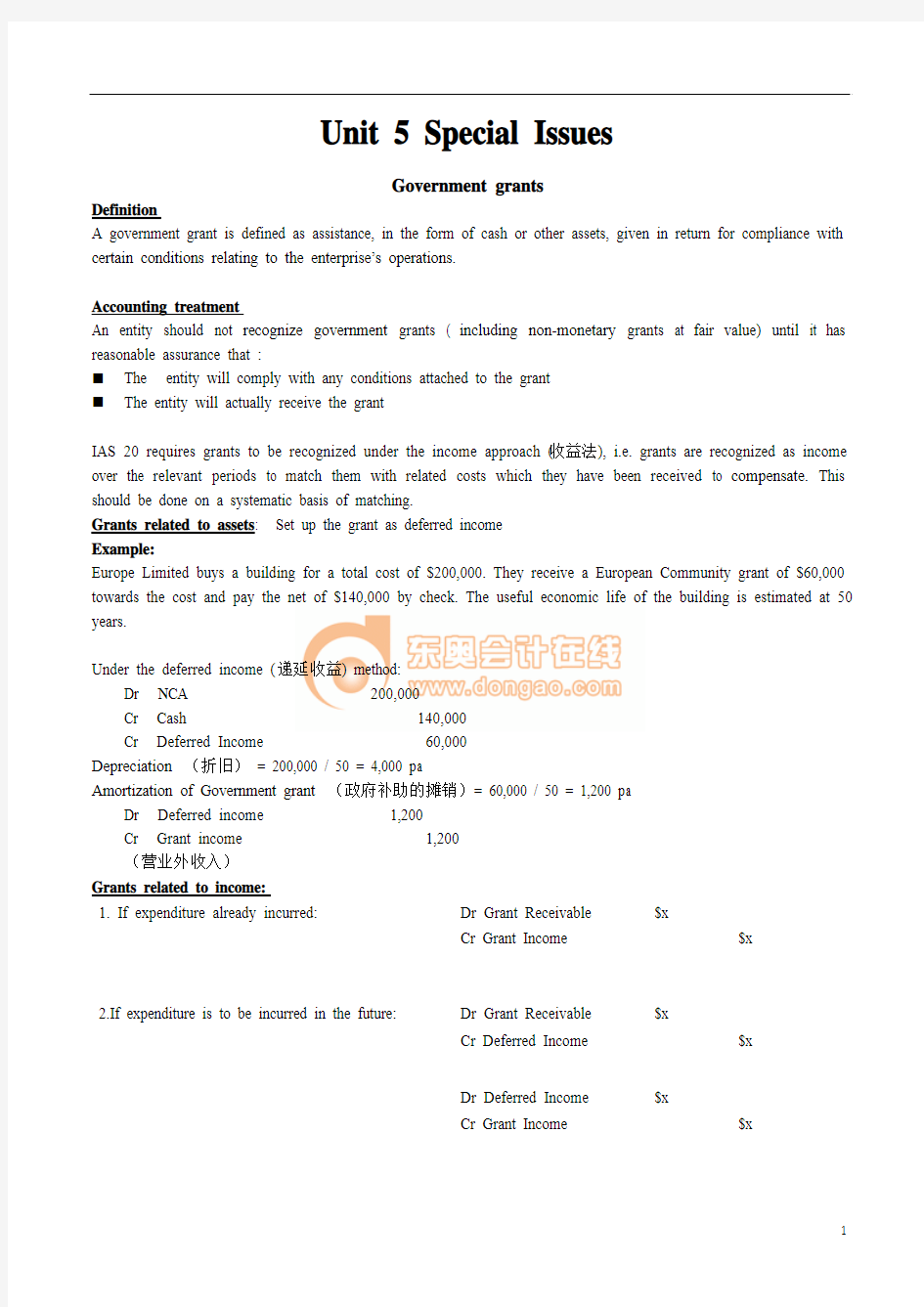

Grants related to assets: Set up the grant as deferred income

Example:

Europe Limited buys a building for a total cost of $200,000. They receive a European Community grant of $60,000 towards the cost and pay the net of $140,000 by check. The useful economic life of the building is estimated at 50 years.

Under the deferred income (递延收益) method:

Dr NCA 200,000

Cr Cash 140,000

Cr Deferred Income 60,000

Depreciation (折旧)= 200,000 / 50 = 4,000 pa

Amortization of Government grant (政府补助的摊销)= 60,000 / 50 = 1,200 pa

Dr Deferred income 1,200

Cr Grant income 1,200

(营业外收入)

Grants related to income:

1. If expenditure already incurred: Dr Grant Receivable $x

Cr Grant Income $x

2.If expenditure is to be incurred in the future: Dr Grant Receivable $x

Cr Deferred Income $x

Dr Deferred Income $x

Cr Grant Income $x

Borrowing costs

Borrowing costs comprise the interest and other costs incurred by an enterprise in borrowing funds:

Interest expense calculated using the effective interest rate

Finance charges in respect of finance leases

Exchange differences

借款费用是企业因借入资金所付出的代价,包括借款利息、折价或者溢价的摊销、辅助费用以及因外币借款而发生的汇兑差额等。承租人确认的融资租赁发生的融资费用属于借款费用。

They may be based on specifically borrowed funds (专门借款)or on the weighted average cost (加权平均成本)of a general borrowings (一般借款).

Qualifying assets are assets that take a substantial period of time to get ready for its intended use or sale.

符合资本化条件的资产是指需要经过相当长时间的构建或者生产活动才能达到预定可使用或者可销售状态的资产。

Accounting treatment

1.Other borrowing costs, such as interest cost on funds borrowed for operations, should be expensed when incurred.

2.Borrowing costs directly incurred on a qualifying asset can be capitalized as part of the cost of that asset.

企业发生的借款费用可直接归属于符合资本化条件的资产构建或者生产的,应当予以资本化,计入相关资产成本。其他借款费用应当在发生时根据其发生额确认为费用,计入当期损益。

Capitalization should:

Start when expenditure on the asset is being incurred, borrowing costs are being incurred and activities are in

progress that are necessary to prepare the asset for its intended use or sale

借款费用允许开始资本化必须同时满足三个条件,即资产支出已经发生、借款费用已经发生、为使资产达到预定可使用或者可销售状态所必要的构建或者生产活动已经开始。

Be suspended when activity development is interrupted

中国:发生非正常中断且中断时间连续超过3个月的,利息费用的资本化应当暂停。

Cease when substantially all the activities necessary to prepare the asset for its intended use or sale are

completed

当使资产达到预定可使用或者可销售状态的生产活动实质上已经完成时,借款费用应当停止资本化。

Income Taxes 所得税

Accounting profits form the basis for computing taxable profits, on which the tax liability for the year is calculated; however, accounting profits and taxable profits are different. There are two reasons for the differences.

Permanent differences. Those occur when certain items revenue or expense are excluded from the computation

of taxable profits.

Temporary differences. Those occur when items of revenue or expense are included in both accounting profits

and taxable profits, but not for the same accounting period. In the long run, the total taxable profits and total accounting profits will be the same so that timing differences originate in one period and are capable of reversal in one or more subsequent periods. Deferred tax is the tax attributable to temporary differences.

Taxable temporary differences, which are temporary differences that will result in taxable amounts in

determining taxable profit ( tax loss) of future periods when the carrying amount of the asset or liability is recovered or settled.

Taxable temporary differences give rise to a deferred tax liability

Deductible temporary differences, which are temporary differences that will result in amounts that are

deductible in determining taxable profit ( tax loss) of future periods when the carrying amount of the asset or liability is recovered or settled.

Deductible temporary differences give rise to a deferred tax asset. Prudence dictates that deferred tax assets can only be recognized when sufficient future taxable profits exist against which they can be utilized.

Deferred tax is an accounting measure used to match the tax effects of transactions with their accounting

impact. It does not represent tax payable to the tax authorities.

Temporary differences are differences between the carrying amount of an asset or liability in the statement of

financial position and its tax base.

Tax base of an asset or liability is the amount attributed to that asset or liability for tax purposes.

计税基础即从税法的角度来看,企业持有的资产、负债的金额。

Tax base of an asset is the amount that will be deductible for tax purposes against any taxable economic benefits that will flow to the enterprise when it recovers the carrying value of the asset.

资产的计税基础,是指在企业收回资产账面价值过程中,计算应纳税所得额时按照税法规定可以自应税经济利益中抵扣的金额,即某一项资产在未来期间计税时可以税前扣除的金额。

Illustration example:

1.A machine cost $10,000. For tax purposes, depreciation of $3,000 has been deducted in the current and prior periods and the remaining cost will be deductible in future periods.

Tax base is $10,000-3,000=$7,000

2.Interest receivable has a carrying amount of $1,000. The related interest revenue will be taxed on a cash basis.

Tax base is nil.

3.Trade receivable have a carrying amount of $10,000. The related revenue has already been included in taxable profit.

Tax base is $10,000.

4.A loan receivable has a carrying amount of $1m. The repayment of the loan will have no tax consequences.

Tax base is $1m.

Tax base of a liability is its carrying amount, less any amount that will be deducted for tax purposes in relation to the liability in future periods.

负债的计税基础,是指负债的账面价值减去未来期间计算应纳税所得额时按照税法规定可予抵扣的金额。

Illustration example:

1.Accrued expenses with a carrying amount of $1,000. The related expense will be deducted for tax purposes on a cash basis.

Tax base is nil.

2.Interest revenue received in advance, with a carrying amount of $10,000. The related interest revenue was taxed on a cash basis.

Tax base is nil.

3.Accrued expenses with a carrying amount of $2,000. The related expense has already been deducted for tax purposes.

Tax base is $2,000.

4.Accrued fines and penalties with a carrying amount of $100. Fines and penalties are not deductible for tax purposes.

Tax base is $100.

5.A loan payable has a carrying amount of $1m. The repayment of the loan will have no tax consequences.

Tax base is $1m.

Recognition of Deferred Tax Liabilities (DTL)

Deferred tax liabilities are the amounts of income taxes payable in future periods in respect of taxable temporary differences.

Formulae:

Carrying Amount of Asset > Tax Base of Asset

?Taxable Temporary Difference x Tax rate = Deferred Tax Liability

?Pay less tax now (more capital allowance available now)

?Pay more tax later (no more capital allowance but company continue to charge depreciation which is added back to taxable profits)

Recognition of Deferred Tax Assets (DTA)

Deferred tax assets are the amounts of income taxes recoverable in future periods in respect of deductible temporary differences.

Formulae:

Carrying Amount of Liability > Tax Base of Liability

?Deductible Temporary Difference x Tax Rate = Deferred Tax Asset

?Pay more tax now (as expenses are not allowable, it will be added back to taxable profit)

?Pay less tax later (in future when the company pays for the expenses, it will be deductive when paid)

Economic benefits in the form of reductions in tax payments will only flow to the organization if it earns sufficient taxable profits against which the deductions can be offset. Therefore an organization only recognizes deferred tax assets when it is probable that taxable profits will be available against which they can be utilized.

递延所得税资产的确认应以未来期间可能取得的应纳税所得额为限。

Accounting policies, changes in accounting estimates and errors

Accounting policies

Accounting policies are the specific principles, bases, conventions, rules and practices adopted by an entity in preparing and presenting financial statements.

An entity must select and apply its accounting policies for a period consistently for similar transactions.

Changes in accounting policies

Accounting policies are normally kept the same from period to period to ensure comparability of financial statements over time.

IAS 8 allows accounting policies to be changed only if:

required by statute or an accounting standard setting body;

the change will result in a more relevant and reliable presentation of events or transactions.

会计政策变更的条件:法律、法规或准则制定机构的要求;会计政策的变更能够提供更可靠、更相关的会计信息。

A change in accounting policy must be applied retrospectively:追溯调整法

Retrospective application means that the new accounting policy is applied to transactions and events as if

it had always been in use.

An adjustment to the opening balance of retained earnings in the statement of changes in equity.

Comparative information should be restated unless it is impracticable to do so

追溯调整法,是指对某项交易或事项变更会计政策,视同该项交易或事项初次发生时即采用变更后的

会计政策,并以此对财务报表相关项目进行调整的方法。采用追溯调整法时,会计政策变更的累计影响数应包括在变更当期期初留存收益中,并调整比较财务报表相关项目。

Changes in accounting estimates

Examples of changes in accounting estimates

the residual value(残值)of non-current assets

the useful lives of non-current assets

the depreciation methods

warranty provisions (质保预计负债)

A change in accounting estimate should be accounted for prospectively.未来适用法

The effects of any change in accounting estimate should be included in the income statement of the period of the change and, if subsequent periods are affected, in those subsequent periods.

如果会计估计的变更仅影响变更当期,有关估计变更的影响应于当期确认;如果会计估计的变更既影响变更当期又影响未来期间,有关估计变更的影响在当期及以后各期确认。

Correction of prior period errors

Prior period errors should be corrected retrospectively.

Practice question:

A change in the estimated useful life of a depreciable asset should be reported

a. prospectively

b. retrospectively

c. either prospectively or retroactively

d. both prospectively and retroactively

Answer: a

Equipment bought by James Steam Generating Company three years ago was charged to equipment expense in error. The cost of the equipment was $100,000, with no expected salvage value, and a 10-year estimated life. James uses the straight-line depreciation method on similar equipment. The error was discovered at the end of year 3 prior to the issuance of James’ financial statements. After correction of the error, the correct carrying value of the equipment will be

a. $30,000.

b. $70,000.

c. $80,000.

d. $100,000.

Answer: b

Events After the Balance Sheet Date

An event, which could be favourable or un-favourable, that occurs between the balance sheet date and the date that the financial statements are authorized for issue.

资产负债表日后事项,是指资产负债表日至财务报告批准报出日之间发生的有利或不利事项。

Adjusting event 调整事项

An event after the balance sheet date that provides further evidence of conditions that existed at the balance sheet. 调整事项是指对资产负债表日已经存在的情况提供了新的或进一步证据的事项。

Non-adjusting event 非调整事项

An event after the balance sheet date that is indicative of a condition that arose after the balance sheet date.

非调整事项是指表明资产负债表日后发生的情况的事项。

Accounting treatment

Adjust financial statements for adjusting events

调整事项应当调整资产负债表日的财务报表。

Do not adjust for non-adjusting events

非调整事项不调整资产负债表日的财务报表。

Non-adjusting events should be disclosed if they are of such importance that non-disclosure would affect the

ability of users to make proper evaluations and decisions. The required disclosure is (a) the nature of the event and (b) an estimate of its financial effect.

非调整事项由于事项重大,对财务报告使用者具有重大影响,如不加以说明,将不利于财务报告使用者作出正确估计和决策,因此,应在附注中对其性质、内容及对财务状况和经营成果的影响加以披露。

If an entity declares dividends after the balance sheet date, the entity shall not recognise those dividends as a

liability at the balance sheet date. That is a non-adjusting event.

资产负债表日后发行股票是非调整事项。

Share based payment

A share based payment is a transaction in which the entity receives or acquires services from employees or other

parties either as consideration for its equity instruments or by incurring liabilities for amounts based on the price of the entity’s shares or other equity instruments of the entity.

股份支付,是指企业为获取职工和其他方提供服务而授予权益工具或承担以权益工具为基础确定的负债的交易。

Equity settled share based payment 以权益结算的股份支付

Cash settled share based payment 以现金结算的股份支付

可行权条件

服务期限条件

Accounting treatment

No accounting treatment at the grant date, except that shares are issued that vest immediately, the expense should be recognised immediately.

除了立即可行权的股份支付外,企业在授予日均不作会计处理。

Alternatively, if there is vesting condition, then cost should be recognised over vesting period. The cost is measured at fair value of the equity instrument at the grant date.

在等待期,计入成本费用的金额应当按照授予日权益工具的公允价值计量并分摊到各期。

If the condition is service condition, the recognition should be based on best estimate of the number of equity instrument expected to vest at year end. The final cost recognised reflects the actual number of equity instrument vesting.

服务期限条件下,在等待期内每个资产负债表日,企业应当以最佳估计的可行权的权益工具数量为依据确认各期应分摊的费用。最终预计可行权权益工具的数量应当与实际可行权工具的数量一致。

If the condition is market performance condition,number of equity instrument is not adjusted even if market condition is not satisfied and options not vested if all other vesting conditions are met (e.g. service condition).

对于附有市场条件的股份支付,只要职工满足了其他所有非市场条件,企业就不再调整权益工具的数量。

In the case of cash-settled share-based payment to purchase service from employees,the entity shall recognise the employee expense and the liability incurred. The entity shall remeasure the fair value of the liability at the end of each reporting period and at the date of settlement, with any changes in fair value recognised in profit or loss for the period.

对于现金结算的涉及职工的股份支付,应当按照每个资产负债表日权益工具的公允价值重新计量,确定成本费用和应付职工薪酬。其后续公允价值变动计入当期损益

Foreign currency translation

Functional currency:the currency of the primary economic environment in which the entity operates.

记账本位币是指企业经营所处的主要经济环境中的货币

Individual level

Foreign currency monetary items (debtors , creditors , cash , loans) must be retranslated using the closing rate. The closing rate is the exchange rate at the balance sheet date. Exchange differences on settlement of monetary items or on retranslating monetary items are recognized in Profit/Loss .

资产负债表日及结算货币性项目时,企业应当采用当日即期汇率折算外币货币性项目,因当日即期汇率与初始确认时或者前一资产负债表日即期汇率不同而产生的汇兑差额,计入当期损益。

Foreign currency non-monetary items (fixed assets , investments , stock) carried at historical cost should be

reported using exchange rate at transaction date, which are not retranslated.

以历史成本计量的外币非货币性项目,已在交易发生日按当日即期汇率折算,资产负债表日不应改变其原记账本位币金额,不产生汇兑差额。

Foreign currency non-monetary items carried at FV should be reported at rate when FV determined. Foreign currency element is not recognised separately. When gain or loss is recognised in Profit/Loss, exchange component is also taken to Profit/Loss. If gain or loss is recognised in equity on a non-monetary asset, any exchange gain is also recognised in equity.

以公允价值计量的外币非货币性项目,期末公允价值以外币反映的,应当先将该外币金额按照公允价值确定当日的即期汇率折算为记账本位币金额,再与原记账本位币金额进行比较。汇率变动的影响不单独计量。作为公允价值变动计入当期损益的,汇率变动也计入当期损益;作为公允价值变动计入权益的,汇率变动也计入权益。

Group level

Where there is an overseas subsidiary that has a functional currency which is a local currency, prior to consolidation it will need to be translated into parent’s currency using the closin g rate method .

The statement of financial position of the overseas entity is translated using the closing rate i.e. the exchange rate at the date of the balance sheet. The income statement items are translated at the average rate for the period.

资产负债表中的资产和负债项目,采用资产负债表日的即期汇率折算,利润表中项目采用平均汇率折算。

With the closing rate method the exchange difference of retranslating the subsidiary’s financial statement is dealt with in equity.

产生的外币财务报表折算差额,在资产负债表中所有者权益项目下单独列示。

Practice question:

According to Statement of F inancial Accounting Standards No. 52, “Foreign Currency Translation,” the assets, liabilities, and operations of a foreign entity are to be measured using that entity’s functional currency. The functional currency of an entity is defined as the currency

a. of the entity’s parent company.

b. of the primary country in which the entity is physically located.

c. in which the books of record are maintained for all entity operations.

d. of the primary economic environment in which the entity operates.

Answer:d

Consolidated financial statement 合并财务报表

重大影响

For the merger of enterprises under the same control, if the consideration of the merging enterprise is that it makes payment in cash, transfers non-cash assets or bear its debts, it shall, on the date of merger, regard the share of the book value of the owner's equity of the merged enterprise as the initial cost of the long-term equity investment. The difference between the initial cost of the long-term equity investment and the payment in cash, non-cash assets transferred as well as the book value of the debts borne by the merging party shall offset against the capital reserve. If the capital reserve is insufficient to dilute, the retained earnings shall be adjusted.

同一控制下的企业合并,合并方以支付现金、转让非现金资产或承担债务方式作为合并对价的,应当

在合并日按照取得被合并方所有者权益账面价值的份额作为长期股权投资的初始投资成本。长期股权投资初始投资成本与支付的现金、转让的非现金资产以及所承担债务账面价值之间的差额,应当调整资本公积(资本溢价或股本溢价);资本公积(资本溢价或股本溢价)不足冲减的,调整留存收益。

If the consideration of the merging enterprise is that it issues equity securities, it shall, on the date of merger, regard the share of the book value of the owner's equity of the merged enterprise as the initial cost of the long-term equity investment. The total face value of the stocks issued shall be regarded as the capital stock, while the difference between the initial cost of the long-term equity investment and total face value of the shares issued shall offset against the capital reserve. If the capital reserve is insufficient to dilute, the retained earnings shall be adjusted.

合并方以发行权益性证券作为合并对价的,应当在合并日按照取得被合并方所有者权益账面价值的份额作为长期股权投资的初始投资成本。按照发行股份的面值总额作为股本,长期股权投资初始投资成本与所发行股份面值总额之间的差额,应当调整资本公积(资本溢价或股本溢价);资本公积(资本溢价或股本溢价)不足冲减的,调整留存收益。发行权益性证券的发行费用应冲减资本公积。

Under the cost method, the dividends or profits declared to distribute by the invested entity shall be recognized as the current investment income.

采用成本法核算的长期股权投资,投资企业应当按照享有被投资单位宣告发放的现金股利或利润确认投资收益。

Under the equity method, If the initial cost of a long-term equity investment is more than the investing enterprise' attributable share of the fair value of the invested entity's identifiable net assets for the investment, the initial cost of the long-term equity investment may not be adjusted. If the initial cost of a long term equity investment is less than the investing enterprise' attributable share of the fair value of the invested entity's identifiable net assets for the investment, the difference shall be included in the current profits and losses and the cost of the long-term equity investment shall be adjusted simultaneously.

在权益法下,长期股权投资的初始投资成本大于投资时应享有被投资单位可辨认净资产公允价值份额的,不调整长期股权投资的初始投资成本;长期股权投资的初始投资成本小于投资时应享有被投资单位可辨认净资产公允价值份额的,应按其差额,借记“长期股权投资”科目,贷记“营业外收入”科目。

After an investing enterprise obtains a long-term equity investment, it shall, in accordance with the attributable share of the net profits or losses of the invested entity, recognize the investment profits or losses and adjust the book value of the long-term equity investment. The investing enterprise shall, in the light of the profits or cash dividends declared to distribute by the invested entity, calculate the proportion it shall obtain, and shall reduce the book value of the long-term equity investment correspondingly.

投资企业取得长期股权投资后,应当按照应享有或应分担的被投资单位实现的净损益份额,确认投资损益并调整长期股权投资的账面价值。投资企业按照被投资单位宣告分派的利润或现金股利计算应分得的股利或利润,相应减少长期股权投资的账面价值。

If Parent company has enough voting power to appoint all the directors of the subsidiary company. P is, in effect, able to manage S as if it were merely a department of P, rather than a separate entity. In strict legal terms P and S remain distinct, but in economic substance they can be regarded as a single unit (a 'group').

如果母公司有足够的投票权来任命子公司所有的董事,那么母公司事实上能够管理子公司,就如同子公司不是一个独立的实体而是母公司的一个部门。从严格的法律形式上看,母公司和子公司是不同的

法律主体,但从经济实质来看,母子公司可以看作一个主体(即集团)。

To reflect the true economic substance of a group of companies we need to produce group accounts in addition to the individual accounts prepared for each company within the group. One of the main methods of doing this is to prepare 'consolidated' accounts. Consolidated accounts present the group as though it were a 'single economic entity'.

为了反应集团公司的真正经济实质,我们除了编制集团中每个公司的个别报表,还需要编制集团报表。集团报表的编制方法之一即合并报表。合并报表视集团为一个经济实体。

Practice question:

On January 1, Jennie Corporation purchased 30% of the common stock of Katlee Company for $500,000. The following information relates to Katlee at the date of acquisition.

Cash $ 50,000

Accounts receivable (net) 250,000

Building (net) 700,000

Land 100,000

Liabilities 100,000

Additional information relating to the purchase appears below.

1. Jennie has the ability to exercise significant influence over Katlee.

2. Both the book value and the fair value are the same for the receivables, land, and liabilities.

3. The fair market value of the building is $900,000.

4. Jennie depreciates its assets on a straight-line basis. Both tangible and intangible assets are amortized over 10 years.

5. For the current year, Katlee had net income of $400,000 and declared and paid dividends of $100,000.

The amount of goodwill related to Jennie’s acquisition of Katlee at January 1 was

a. Zero.

b. $60,000.

c. $140,000.

d. $200,000.

Answer: c {500-(50+250+900+100-100)×30%}

The course summary

Introduction

Financial Statement Elements

Special Issues

有关会计科目的中英文对照

一级科目二级科目三级科目四级科目 代码名称代码名称代码名称代码名称英译 1 资产assets 11~ 12 流动资产current assets 111 现金及约当现金cash and cash equivalents 1111 库存现金cash on hand 1112 零用金/周转金petty cash/revolving funds 1113 银行存款cash in banks 1116 在途现金cash in transit 1117 约当现金cash equivalents 1118 其它现金及约当现金other cash and cash equivalents 112 短期投资short-term investments 1121 短期投资-股票short-term investments - stock 1122 短期投资-短期票券short-term investments - short-term notes and bills 1123 短期投资-政府债券short-term investments - government bonds 1124 短期投资-受益凭证short-term investments - beneficiary certificates 1125 短期投资-公司债short-term investments - corporate bonds 1128 短期投资-其它short-term investments - other 1129 备抵短期投资跌价损失allowance for reduction of short-term investment to market 113 应收票据notes receivable 1131 应收票据notes receivable 1132 应收票据贴现discounted notes receivable 1137 应收票据-关系人notes receivable - related parties 1138 其它应收票据other notes receivable 1139 备抵呆帐-应收票据allowance for uncollec- tible accounts- notes receivable 114 应收帐款accounts receivable 1141 应收帐款accounts receivable 1142 应收分期帐款installment accounts receivable 1147 应收帐款-关系人accounts receivable - related parties 1149 备抵呆帐-应收帐款allowance for uncollec- tible accounts - accounts receivable 118 其它应收款other receivables 1181 应收出售远汇款forward exchange contract receivable 1182 应收远汇款-外币forward exchange contract receivable - foreign currencies 1183 买卖远汇折价discount on forward ex-change contract 1184 应收收益earned revenue receivable 1185 应收退税款income tax refund receivable 1187 其它应收款- 关系人other receivables - related parties 1188 其它应收款- 其它other receivables - other 1189 备抵呆帐- 其它应收款allowance for uncollec- tible accounts - other receivables 121~122 存货inventories 1211 商品存货merchandise inventory 1212 寄销商品consigned goods 1213 在途商品goods in transit 1219 备抵存货跌价损失allowance for reduction of inventory to market

会计专业英语重点1

Unit 1 Financial information about a business is needed by many outsiders .These outsiders include owners, bankers, other creditors, potential investors, labor unions, government agencies ,and the public ,because all these groups have supplied money to the business or have some other interest in the business that will be served by information about its financial position and operating results. 许多企业外部的人士需要有关企业的财务信息,这些外部人员包括所有者、银行家、其他债权人、潜在投资者、工会、政府机构和公众,因为这些群体对企业投入了资金,或享有某些利益,所以必须得到企业财务状况和经营成果信息。 Unit 2 Each proprietorship, partnership, and corporation is a separate entity. 每一独资企业、合伙企业和股份公司都是一个单独的主体。 In accrual accounting, the impact of events on assets and equities is recognized on the accounting records in the time periods when services are rendered or utilized instead of when cash is received or disbursed. That is revenue is recognized as it is earned, and expenses are recognized as they are incurred –not when cash changes hands .if the cash basis accounting were used instead of the accrual basis, revenue and expense recognition would depend solely on the timing of various cash receipts and disbursements. 在权责发生制下,视服务的提供而非现金的收付在本期对资产和权益的影响作出会计记录。即,收入是在赚取时确认,费用是在发生时确认——而不是在现金转手时。如果现金收付制替代权责发生制,那么收入和费用仅仅依靠各种现金收付活动的时间确定来确认。 Unit 3 During each accounting year ,a sequence of accounting procedures called the accounting cycle is completed. 在每一会计年度内,要依次完成被称为会计循环的会计程序。 Transactions are analyzed on the basis of the business documents known as source documents and are recorded in either the general journal or the special journal, i. e . the sales journal ,the purchases journal (invoice register ) ,cash receipts journal and cash disbursements journal . 根据业务凭证即原始凭证分析各项交易,并记入普通日记账或特种日记账,也就是销货日记账,购货日记账(发票登记簿),现金收入日记账和现金支出日记账。 A trial balance is prepared from the account balance in the ledger to prove the equality of debits and credits. 根据分类账户的余额编制试算平衡表,借以验证借项和贷项是否相等。 A T-account has a left-hand side and a right-hand side, called respectively the debit side and credit side. 一个T 型账户有左方和右方,分别称做借方和贷方。 After transactions are entered ,account balance (the difference between the sum of its debits and the sum of its credits ) can be computed.

会计专业英语期末试题 )

期期末测试题 Ⅰ、Translate The Following Terms Into Chinese 、 1、entity concept 主题概念 2、depreciation折旧 3、double entry system 4、inventories 5、stable monetary unit 6、opening balance 7、current asset 8、financial report 9、prepaid expense 10、internal control 11、cash flow statement 12、cash basis 13、tangible fixed asset 14、managerial accounting 15、current liability 16、internal control 17、sales return and allowance 18、financial position 19、balance sheet 20、direct write-off method Ⅱ、Translate The Following Sentences Into Chinese 、 1、Accounting is often described as an information system、It is the system that measures business activities, processes into reports and communicates these findings to decision makers、 2、The primary users of financial information are investors and creditors、Secondary users include the public, government regulatory agencies, employees, customers, suppliers, industry groups, labor unions, other companies, and academic researchers、 3、There are two sources of assets、One is liabilities and the other is owner’s equity、Liabilities are obligations of an entity arising from past transactions or events, the settlement of which may result in the transfer or use of assets or services in the future、 资产有两个来源,一个就是负债,另一个就是所有者权益。负债就是由过去得交易或事件产生得实体得义务,其结算可能导致未来资产或服务得转让或使用。 4、Accounting elements are basic classification of accounting practices、They are essential units to present the financial position and operating result of an entity、In China, we have six groups of accounting elements、They are assets, liabilities, owner’s equity, revenue, expense and profit (income)、会计要素就是会计实践得基础分类。它们就是保护财务状况与实体经营

会计科目英文缩写

一、企业财务会计报表封面FINANCIAL REPORT COVER 报表所属期间之期末时间点Period Ended 所属月份Reporting Period 报出日期Submit Date 记账本位币币种Local Reporting Currency 审核人Verifier 填表人Preparer 记账符号 DR:debit record (借记) CR:credit recrod(贷记) 二、资产负债表Balance Sheet 资产Assets 流动资产Current Assets 货币资金Bank and Cash 短期投资Current Investment 一年内到期委托贷款Entrusted loan receivable due within one year 减:一年内到期委托贷款减值准备Less: Impairment for Entrusted loan receivable due within one year 减:短期投资跌价准备Less: Impairment for current investment 短期投资净额Net bal of current investment 应收票据Notes receivable 应收股利Dividend receivable 应收利息Interest receivable

应收账款Account receivable 减:应收账款坏账准备Less: Bad debt provision for Account receivable 应收账款净额Net bal of Account receivable 其他应收款Other receivable 减:其他应收款坏账准备Less: Bad debt provision for Other receivable 其他应收款净额Net bal of Other receivable 预付账款Prepayment 应收补贴款Subsidy receivable 存货Inventory 减:存货跌价准备Less: Provision for Inventory 存货净额Net bal of Inventory 已完工尚未结算款Amount due from customer for contract work 待摊费用Deferred Expense 一年内到期的长期债权投资Long-term debt investment due within one year 一年内到期的应收融资租赁款Finance lease receivables due within one year 其他流动资产Other current assets 流动资产合计Total current assets 长期投资Long-term investment 长期股权投资Long-term equity investment 委托贷款Entrusted loan receivable 长期债权投资Long-term debt investment 长期投资合计Total for long-term investment 减:长期股权投资减值准备Less: Impairment for long-term equity investment 减:长期债权投资减值准备Less: Impairment for long-term debt investment

会计专业英语翻译

. 1. Accounting first is an economic calculation. Economic calculation includes both static phenomenon on the economy's stock of the situation, including the situation of the period of dynamic flow, including both pre-calculated plan, but also after the actual calculation. Accounting is a typical example of economic calculation, calculation of economic calculation in addition to accounting, which includes statistical computing and business computing. 2. Accounting is an economic information systems. It would be a company dispersed into the business activities of a group of objective data, providing the company's performance, problems, and enterprise funds, labor, ownership, income, costs, profits, debt, and other information. Clearly, the accounting is to provide financial information-based economy information systems, business is the licensing of a points, thus accounting has been called "corporate language." 3. Accounting is an economic management.The accounting is social production develops to a certain stage of the product development and production is to meet the needs of the management, especially with the development of the commodity economy and the emergence of competition in the market through demand management on the economy activities strict control and supervision. At the same time, the content and form of accounting constantly improve and change, from a purely accounting, scores, mainly for accounting operations, external submit accounting statements, as in prior operating forecasts, decision-making, on the matter of economic activities control and supervision, in hindsight, check. Clearly, accounting whether past, present or future, it is people's economic management activities.

八年级下册英语第四单元译文

八年级下册英语第四单元译文 P26,2d 分角色表演对话。 戴夫:金,你看上去很难过。怎么了? 金:嗯,昨天我发现我的妹妹翻阅我的东西。她拿走了我的一些新杂志和光盘。戴夫:嗯……这很不好。她还给你了吗? 金:是的,但是我还是对她很生气。我该怎么办? 戴夫:嗯,我想你可以告诉她,让她道歉。但你为什么不忘了它呢? " 那样你们还能做朋友。虽然她错了,但这没什么大不了的。金:你说得对。谢谢你的建议。 戴夫:不客气。希望事情会好起来。 P27 Section A 3a 亲爱的鸿特先生, 我的问题是我不能和我家人相处。我父母间的关系变得很困难。他们经常打架,我真的不喜欢那样。打架是他们唯一拥有的交流方式。我不知道是否我应该对他们说些什么关于这个问题。他们吵架的时候就像一大片黑色的云笼罩在我们家。我的哥哥对我也不是很好。他经常拒绝让我看我最喜欢的电视节目。相反,他可以看任何他喜欢的直到深夜。我认为这是不公平的。在家我经常感觉孤独和紧张。那正常吗?我能够做什么?一个伤心的十三岁的孩子 亲爱的正在伤心的十三岁的孩子, 在你这个年龄总是不容易的,有这些感觉也是正常的。为什么你不和你的家人谈论你的这些感觉呢?如果你的父母间有问题,你应该帮助他们。或许你在家可以多做些家务,让你的父母有更多的时间可以进行适当的交流。其次,你为什么不坐下来和你哥哥谈谈呢?你应该向他解释你不介意他一直看电视。但是他应该让你看你最喜欢的节目。我

希望事情将很快会变好。鸿特先生 P28 语法聚焦 你看起来很累。怎么了?昨晚我一直学习到半夜,因此睡眠不足。我该怎么办?你为什么不忘掉它呢?虽然她错了,但这没什么大不了的。他应该做些什么?他应该跟他的朋友谈一谈,以便他可以说他很抱歉。也许你可以去他家。我想我可以,但我不想让他吃惊。 P30 2b 也许你应该学会放松!近来,中国的孩子有时周末比上学日更忙,因为他们不得不上许多课外辅导班。他们中的许多人正在学习考试技能以便能进人一所好的高中,以后考上好大学。其他的学生在练习体育,以便可以参加竞赛并获胜。然而,这并不仅仅发生在中国。泰勒一家是个典型的美国家庭。凯茜?泰勒的三个孩子的生活很忙碌。凯茜说,“放学后,大部分的日子里我带两个儿子中的一个去练习篮球,带我的女儿去进行足球训练。然后,我要带另个一个儿子去上钢琴课。也许我能减少一些他们的活动,但我相信,这些活动对孩子们的未来是很重要的。我真的希望他们能够成功。”然而,疲惫不堪的孩子们直到晚上七点后才回家。他们很快吃完晚饭,然后就到做作业的时间了。琳达?米勒是一位三个孩子的母亲,她了解这样的压力。“在一些家庭中,竞争从很小就开始了,一直持续到子们长大她说,“妈妈们把孩子们送去上各种各样的课程。他们总是把他们和其他孩子比较。这太疯狂了。我认为这是不公平的。他们为什么不让孩子做回孩子呢?人们不应该对自己的孩子这么苛刻。” 医生说,太多的压力不利于孩子的发展。爱丽丝?格林医生说,所有这些活动都会给孩子造成很大的压力。“孩子们也应该有时间放松和独立思考。虽然想让孩子成功是正常的,但是拥有快乐的孩子更重要。”

新准则会计科目英文翻译

新准则会计科目英文翻译 一、资产类 1 1001 库存现金cash on hand 2 1002 银行存款bank deposit 5 1015 其他货币资金other monetary capital 9 1101 交易性金融资产transaction monetary assets 11 1121 应收票据notes receivable 12 1122 应收账款Account receivable 13 1123 预付账款account prepaid 14 1131 应收股利dividend receivable 15 1132 应收利息accrued interest receivable 21 1231 其他应收款accounts receivable-others 22 1241 坏账准备had debts reserve 28 1401 材料采购procurement of materials 29 1402 在途物资materials in transit 30 1403 原材料raw materials 32 1406 库存商品commodity stocks 33 1407 发出商品goods in transit 36 1412 包装物及低值易耗品wrappage and low value and easily wornout articles 42 1461 存货跌价准备reserve against stock price declining 43 1501 待摊费用fees to be apportioned 45 1521 持有至到期投资hold investment due 46 1522 持有至到期投资减值准备hold investment due reduction reserve 47 1523 可供出售金融资产financial assets available for sale 48 1524 长期股权投资long-term stock ownership investment 49 1525 长期股权投资减值准备long-term stock ownership investment reduction reserve 50 1526 投资性房地产investment real eastate 51 1531 长期应收款long-term account receivable 52 1541 未实现融资收益unrealized financing income 54 1601 固定资产permanent assets 55 1602 累计折旧accumulated depreciation 56 1603 固定资产减值准备permanent assets reduction reserve 57 1604 在建工程construction in process 58 1605 工程物资engineer material 59 1606 固定资产清理disposal of fixed assets 60 1611 融资租赁资产租赁专用financial leasing assets exclusively for leasing 61 1612 未担保余值租赁专用unguaranteed residual value exclusively for leasing 62 1621 生产性生物资产农业专用productive living assets exclusively for agriculture 63 1622 生产性生物资产累计折旧农业专用productive living assets accumulated depreciation exclusively for agriculture 64 1623 公益性生物资产农业专用non-profit living assets exclusively for agriculture 65 1631 油气资产石油天然气开采专用oil and gas assets exclusively for oil and gas exploitation 66 1632 累计折耗石油天然气开采专用accumulated depletion exclusively for oil and gas exploitation 67 1701 无形资产intangible assets 68 1702 累计摊销accumulated amortization

(完整版)会计专业英语重点词汇大全

?accounting 会计、会计学 ?account 账户 ?account for / as 核算 ?certified public accountant / CPA 注册会计师?chief financial officer 财务总监?budgeting 预算 ?auditing 审计 ?agency 机构 ?fair value 公允价值 ?historical cost 历史成本?replacement cost 重置成本?reimbursement 偿还、补偿?executive 行政部门、行政人员?measure 计量 ?tax returns 纳税申报表 ?tax exempt 免税 ?director 懂事长 ?board of director 董事会 ?ethics of accounting 会计职业道德?integrity 诚信 ?competence 能力 ?business transaction 经济交易?account payee 转账支票?accounting data 会计数据、信息?accounting equation 会计等式?account title 会计科目 ?assets 资产 ?liabilities 负债 ?owners’ equity 所有者权益 ?revenue 收入 ?income 收益

?gains 利得 ?abnormal loss 非常损失 ?bookkeeping 账簿、簿记 ?double-entry system 复式记账法 ?tax bearer 纳税人 ?custom duties 关税 ?consumption tax 消费税 ?service fees earned 服务性收入 ?value added tax / VAT 增值税?enterprise income tax 企业所得税?individual income tax 个人所得税?withdrawal / withdrew 提款、撤资?balance 余额 ?mortgage 抵押 ?incur 产生、招致 ?apportion 分配、分摊 ?accounting cycle会计循环、会计周期?entry分录、记录 ?trial balance试算平衡?worksheet 工作草表、工作底稿?post reference / post .ref过账依据、过账参考?debit 借、借方 ?credit 贷、贷方、信用 ?summary/ explanation 摘要?insurance 保险 ?premium policy 保险单 ?current assets 流动资产 ?long-term assets 长期资产 ?property 财产、物资 ?cash / currency 货币资金、现金

会计专业英语期末考试练习卷(new)

会计专业英语期末考试练习卷(new)

1. The economic resources of a business are called : B A. Owner ’s Equity B. Assets C. Accounting equation D. Liabilities 2. DTK Company has a $3500 accounts receivable from GRS Company. On January 20, GRS Company makes a partial payment of $210 0 to DTK Company. The journal entry made on January 20 by DTK Company to record this transaction includes: D A. A debit to the cash receivable account of $2100. B. A credit to the accounts receivable account of $2100. C. A debit to the cash account of $1400. D. A debit to the accounts receivable account of $1400. 3. In general terms, financial assets appear in the balance sheet at: A A. Face value. 账面价值 B. Current value. 现值 C. Market value. 市场价值 D. Estimated future sales value. 4. Each of the following measures strengthens intern al control over cash receipts except : D A. The use of a voucher system. B. Preparation of a daily listing of all checks received through the mail. C. The deposit of cash receipts intact in the bank on a daily basis. D. The use of cash registers. 5. Which of the following items is the greatest in dollar amount? D A. Beginning inventory B. Cost of goods sold. C. Cost of goods available for sale D. Ending inventory 6. Why do companies prefer the LIFO inventory 后进先出法method during a period of rising prices? B A. Higher reported income B. Lower income taxes C. Lower reported income D. Higher ending inventory 7. Which of the following characteristics would prevent an item from being included in the classification of plant and equipment? D A. Intangible

会计科目英文翻译

-! 会计科目英文翻译 一、资产类 Assets 流动资产 Current assets 货币资金 Cash and cash equivalents 1001 现金 Cash 1002 银行存款 Cash in bank 1009 其他货币资金 Other cash and cash equivalents '100901 外埠存款 Other city Cash in bank '100902 银行本票 Cashier's cheque '100903 银行汇票 Bank draft '100904 信用卡 Credit card '100905 信用证保证金 L/C Guarantee deposits '100906 存出投资款 Refundable deposits 1101 短期投资 Short-term investments '110101 股票 Short-term investments - stock '110102 债券 Short-term investments - corporate bonds '110103 基金 Short-term investments - corporate funds '110110 其他 Short-term investments - other 1102 短期投资跌价准备 Short-term investments falling price reserves 应收款 Account receivable 1111 应收票据 Note receivable 银行承兑汇票 Bank acceptance 商业承兑汇票 Trade acceptance 1121 应收股利 Dividend receivable 1122 应收利息 Interest receivable 1131 应收账款 Account receivable 1133 其他应收款 Other notes receivable 1141 坏账准备 Bad debt reserves 1151 预付账款 Advance money 1161 应收补贴款 Cover deficit by state subsidies of receivable 库存资产 Inventories 1201 物资采购 Supplies purchasing 1211 原材料 Raw materials 1221 包装物 Wrappage 1231 低值易耗品 Low-value consumption goods 1232 材料成本差异 Materials cost variance 1241 自制半成品 Semi-Finished goods 1243 库存商品 Finished goods 1244 商品进销差价 Differences between purchasing and selling price 1251 委托加工物资 Work in process - outsourced 1261 委托代销商品 Trust to and sell the goods on a commission basis 1271 受托代销商品 Commissioned and sell the goods on a commission basis 1281 存货跌价准备 Inventory falling price reserves 1291 分期收款发出商品 Collect money and send out the goods by stages 1301 待摊费用 Deferred and prepaid expenses 长期投资 Long-term investment 1401 长期股权投资 Long-term investment on stocks '140101 股票投资 Investment on stocks '140102 其他股权投资 Other investment on stocks 1402 长期债权投资 Long-term investment on bonds '140201 债券投资 Investment on bonds '140202 其他债权投资 Other investment on bonds 1421 长期投资减值准备 Long-term investments depreciation reserves 股权投资减值准备 Stock rights investment depreciation reserves 债权投资减值准备 Bcreditor's rights investment depreciation reserves

《财会专业英语》期末试卷及答案

《财会专业英语》期终试卷 I.Put the following into corresponding groups. (15 points) 1.Cash on hand 2.Notes receivable 3.Advances to suppliers 4. Other receivables 5.Short-term loans 6.Intangible assets 7.Cost of production 8.Current year profit 9. Capital reserve 10.Long-term loans 11.Other payables 12. Con-operating expenses 13.Financial expenses 14.Cost of sale 15. Accrued payroll II.Please find the best answers to the following questions. (25 Points) 1. Aftin Co. performs services on account when Aftin collects the account receivable A.assets increase B.assets do not change C.owner’s equity d ecreases D.liabilities decrease 2. A balance sheet report . A. the assets, liabilities, and owner’s equity on a particular date B. the change in the owner’s capital during the period C. the cash receipt and cash payment during the period D. the difference between revenues and expenses during the period 3. The following information about the assets and liabilities at the end of 20 x 1 and 20 x 2 is given below: 20 x 1 20 x 2 Assets $ 75,000 $ 90,000 Liabilities 36,000 45,000 how much the owner’sequity at the end of 20 x 2 ? A.$ 4,500 B.$ 6,000 C.$ 45,000 D.$ 43,000

财务管理专业英语期末复习

财务管理专业英语期末重点 一、单词 Topic1 财务管理financial management 资本预算capital budgeting 资本结构capital structure 股利政策dividend policy 存货inventory 风险规避risk aversion 股东权益stockholder s’ equity 流动负债current liability Topic2 财务风险financial risk 合伙制企业partnership 私人业主制企业sole proprietorship 收入revenue 主计长controller 财务困境financial distress 股票期权stock option 首次公开发行股票(IPO) initial public offering Topic 3 盈利能力profitability 偿付能力solvency 利润表income statement 有价证券marketable securities 提款withdrawal 应收账款accounts receivable 递延税款deferred tax Topic4 流动性比率liquidity ratio 权益乘数equity multiplier 资产收益率(ROA) return on assets 毛利gross profit margin 权益报酬率return on equity 市盈率P/E ratio 杠杆比率leverage ratio 息税前盈余(EBIT) earnings before interest and taxes Topic5 货币时间价值time value of money 年金annuity 折现率discount rate 机会成本opportunity cost

相关文档

- 会计专业英语期末试题 )

- 《财会专业英语》期末试卷及答案

- 会计专业英语期末试题 )知识讲解

- 《会计专业英语》期末复习资料

- 会计专业英语重要词汇(完成)

- [南开大学]《会计专业英语》19秋期末考核(答案参考)

- 《财会专业英语》期末试卷及答案

- 中国地质大学(北京)《会计专业英语》期末考试拓展学习(七)

- 会计专业英语期末试题 )

- 会计专业英语期末考试练习卷(new)

- 英文会计期末试卷

- 会计专业英语期末考试练习卷(new)

- 会计英语专业词汇

- 《会计专业英语》期末复习资料

- 会计专业英语期末试题)

- 财会专业英语期末试卷及答案

- 会计专业英语练习题

- 财务管理专业英语期末复习

- 会计专业英语期末试题

- 会计英语试卷