会计英语课后题答案Answer for lesson4

Exercise

4.1 Select the best answer for each of the following unrelated items

1. C. This is not a business combination as control has not been achieved given Mr. Bill's veto power. XYZ has significant influence and should account for this investment using the equity method.

2. A. When control exists, the parent must consolidate the subsidiary.

3. B. This is the acquisition method; it includes 100% of the fair value of the subsidiary.

4. B. The subsidiary’s shares are eliminated upon consolidation.

5. C. 600,000 + 1,432,000 – 56,000 – 45,000 + 120,000 = 2,051,000.

6. C. Undepreciated goodwill = €80,000 –20,000 = €60,000.

7. C. Net income using the equity method is the same as consolidated net income, except that it is reported on one line.

8. B. Cost and equity methods are the two acceptable methods to record investment transactions.

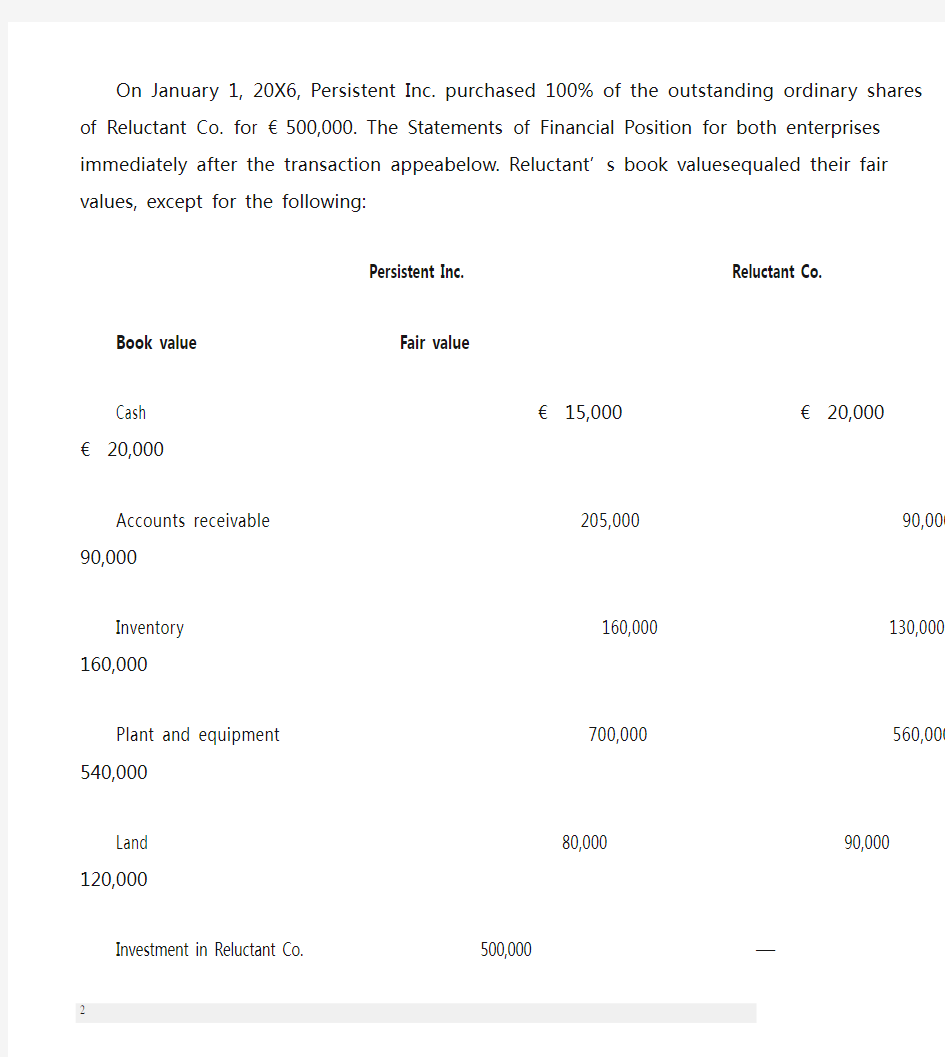

4.2 Consolidation of 100% owned subsidiaries at the date of acquisition

On January 1, 20X6, Persistent Inc. purchased 100% of the outstanding ordinary shares of Reluctant Co. f or €500,000. The Statements of Financial Position for both enterprises immediately after the transaction appear below. Reluctant’s book values equaled their fair values, except for the following:

Persistent Inc. Reluctant Co.

Book value Fair value

Cash € 15,000€ 20,000 € 20,000 Accounts receivable 205,000 90,000 90,000 Inventory 160,000 130,000 160,000

Plant and equipment 700,000 560,000 540,000

Land 80,000 90,000 120,000 Investment in Reluctant Co. 500,000 —

Goodwill — 25,000 —

€ 1,660,000 € 915,000

Accounts payable € 250,000 € 170,000 170,000

Long-term debt 640,000 440,000 450,000 Ordinary shares 350,000 240,000

Retained earnings 420,000 65,000

€ 1,660,000€ 915,000

Enquired

Prepare consolidated financial statements for Persistent Inc. immediately after its acquisition of Reluctant Co., using the direct method.

Calculation and allocation of purchase discrepancy

Cost of investment in Reluctant Co.: € 500,000

Notice that goodwill that existed on Reluctant’s books at the date of acquisition had a fair value of €0 at the date of acquisition. The amount provides evidence of a previous acquisition of another enterprise by Reluctant. From Persistent’s point of view, this intangible asset has no value and represents a decrease in Reluctant’s net asset value. This issue will be covered in more depth in the next topic.

4.3Consolidation less than 100% owned subsidiaries after the date of acquisition using working paper approach On January 1, 20X5, Pascal Ltd. purchased 90% of Socrates Co. for €1,655,000 cash. At that time, Socrates had the following Statement of Financial Position.

SOCRATES CO.

Statement of Financial Position

At January 1, 20X5

Book value Fair value

Cash € 165,000€ 165,000

Accounts receivable 285,000 270,000

Inventory 300,000 345,000

Plant and equipment — Net 2,250,000 2,400,000

€ 3,000,000

Accounts payable € 270,000 270,000

Long-term debt 1,200,000 1,150,000

Ordinary shares 600,000

Retained earnings 930,000

€ 3,000,000

The long-term debt is payable in 10 years. The plant and equipment have an average remaining useful life of 10 years and are being depreciated on a straight-line basis. The annual goodwill impairment tests revealed a €2,000 loss in 20X5 and a €5,100 loss in 20X6. (These losses pertain to Pascal’s 90% ownership of Socrates. As such, the full amounts should be deducted from the consolidated earnings.) The following occurred in 20X5: Socrates earned €1,300,000 and paid dividends of €75,000.

Pascal uses the equity method to record its investment in Socrates but must report on a consolidated basis. At December 31, 20X6, the following financial statements were available:

Statements of Financial Position

At December 31, 20X6

Pascal Socrates

Cash € 371,600€ 239,000

Accounts receivable 252,500 517,500

Inventory 1,455,000 562,500

Plant and equipment — Net 3,946,500 2,994,500

Investment in subsidiary 2,876,400

€ 8,902,000€ 4,313,500

Accounts payable € 675,000€ 73,500

Long-term debt — 1,200,000

Future income taxes 160,000 75,000

Ordinary shares 1,500,000 600,000

Retained earnings 6,567,000 2,365,000

€ 8,902,000€ 4,313,500

Statements of Income and Retained Earnings

For the year ended December 31, 20X6

Pascal Socrates

Sales €14,609,550€ 2,475,000

Investment income 183,900 —

Other income — 100,000

Cost of sales 11,500,000 1,710,000

Depreciation 159,000 156,000

Other expenses 606,750 421,500

Income tax expense 506,250 57,500

12,772,000 2,345,000

Net income 2,021,450 230,000

Beginning balance, retained earnings 5,045,550 2,155,000

Dividends (500,000) (20,000)

Ending balance, retained earnings € 6,567,000 € 2,365,000

Assume that Pascal elects to value the non-controlling interest in Socrates’ at the NCI’s percentile interest in the identifiable net assets of the subsidiary.

Required

1. Complete the calculation and allocation of purchase discrepancy and non-controlling interest.

2. Complete the purchase discrepancy and adjustment schedule.

3. Prepare eliminating entries for 20X6. Be sure to include appropriate commentary in support of each entry. Solution:

1. Calculation and allocation of purchase discrepancy and non-controlling interest

Cost of 90% of Socrates at January 1, 20X5 € 1,655,000

Fair value of identifiable net assets

(€1,760,000 ×90%) 1,584,000

Balance — Goodwill € 71,000

Purchase discrepancy allocated to

Accounts receivable –15,000

Inventory 45,000

Plant and equipment 150,000

Long term debt 50,000 € 230,000

TOTAL € 301,000

Non-controlling interest: €1,760,000 ×10% = €176,000

2.

Purchase discrepancy adjustment schedule

3. Eliminating entries

#1 Investment income (230,000 ×90% – 23,100) ............ 183,900

Dividends — S ........................................................ 18,000

Investment in subsidiary ......................................... 165,900

To eliminate 20X6 equity basis investment income and the parent’s share of Socrates’ 20X6 dividends against the investment account

#2 Ordinary shares ............................................................. 600,000

Retained earnings, January 1, 20X6 ............................. 2,155,000

Purchase discrepancy .................................................... 249,000

Investment in subsidiary ......................................... 2,710,500

Non-controlling interest .......................................... 293,500

To eliminate start-of-the-year retained earnings and ordinary shares of Socrates against the start-of-the-year balance of the investment account and to establish the purchase discrepancy and non-controlling interest at the end of December 31, 20X5

#3 Other expenses (interest) .............................................. 5,000

Depreciation expense .................................................... 15,000

Goodwill impairment loss ............................................ 5,100

Plant and equipment ..................................................... 120,000

Goodwill ....................................................................... 63,900

Long-term debt ............................................................. 40,000

Purchase discrepancy .............................................. 249,000

To allocate the purchase discrepancy amount at the end of 20X5, to record depreciation of purchase discrepancies for 20X6, and to set up the undepreciated purchase discrepancy balances at the end of 20X6

#4 Non-controlling interest — I/S ..................................... 21,000

Non-controlling interest — SFP ............................. 21,000

To allocate the non-controlling interest’s share of 20X6 net income

#5 Non-controlling interest — SFP ................................... 2,000

Dividends — I/S ..................................................... 2,000

To allocate non-controlling interest’s percentage of dividends paid by Socrates in 20X6

4.4Consolidation less than 100% owned subsidiaries after the date of acquisition using direct method and working paper method

On January 1, 20X2, Ping Inc. acquired 75% of Sing Co. for €1,500,000. Sing’s condensed balance sheet and fair values immediately before the acquisition were as follows:

SING CO. Statement of Financial Position

At December 31, 20X1

Book value Fair value

Cash and accounts receivable € 540,000 € 540,000

Inventory 250,000 270,000

Plant and equipment (net) 1,435,000 1,575,000

€ 2,225,000 € 2,385,000

Current liabilities € 785,000€785,000

Ordinary shares 1,200,000

Retained earnings 240,000

€ 2,225,000

?Sing’s inventory turns over 6 times in a year.

?Plant and equipment have an estimated useful life of 10 years.

?Ping’s annual goodwill impairment test revealed a €30,000 loss for 20X3. The impairment is attributed to economic decline.

?On December 31, 20X3, Ping owes Sing €18,000 related to an intercompany interest-free loan.

The separate entity financial statements for the two companies at December 31, 20X3, are as follows:

Income Statements

For the year ended December 31, 20X3

PING SING

Sales € 3,600,000€ 2,800,000

Investment income 237,000 —

Total revenue 3,837,000 2,800,000

Cost of goods sold 1,600,000 1,500,000

Amortization expense 294,000 730,000

Administration and other expenses 600,000 200,000

Total expenses 2,494,000 2,430,000

Net income € 1,343,000€ 370,000

Statements of Changes in Equity

For the year ended December 31, 20X3

Balance, January 1 — Retained earnings € 2,504,000€ 1,546,000

Net income 1,343,000 370,000

3,847,000 1,916,000

Dividends 400,000 200,000

Balance, December 31 — Retained earnings € 3,447,000€ 1,716,000

Statements of Financial Position

At December 31, 20X3

Cash € 100,000€ 40,000

Accounts receivable 960,000 840,000

Inventory 1,200,000 500,000

Plant and equipment (net) 1,914,000 1,956,000

Investment in Sing Co. 2,541,000 —

€ 6,715,000€ 3,336,000

Current liabilities € 1,068,000€ 420,000

Ordinary shares 2,200,000 1,200,000

Retained earnings 3,447,000 1,716,000

€ 6,715,000€ 3,336,000

Additional information:

(1) Company PING selected to value the NCI at NCI’s share of the fair value of the identifiable net asset of Sing.

(2) Parent amortizes 100% of goodwill, FVI is amortized according to the proportionate share the parent and NCI own Required

1. Prepare the Year 3 consolidated statements for Ping Inc. for the year ended December 31, Year 3, using the direct approach.

2. Prepare a schedule of the changes in non-controlling interest since acquisition.

3. Prepare the five entries necessary for the working paper approach and provide descriptions.

Solutions:

1.

学术英语 课文翻译

U8 A 1 在过去的30年里,作为一个专业的大提琴演奏家,我花了相当于整整20年时间在路上执行和学习音乐传统和文化。我的旅行使我相信在我们的全球化的世界中,文化传统来自于一个身份、社会稳定和富有同情心的互动的基本框架。 2 世界在快速改变,正如我们一定会创造不稳定的文化,让人质疑他们的地方。全球化使我们服从于别人的规则,这往往会威胁到个人的身份。这自然使我们紧张,因为这些规则要求我们改变传统习惯。所以如今全球领导者的关键问题是:如何使习惯和文化发展到融入更大的行星,同时不必牺牲鲜明特色和个人的骄傲? 3 我的音乐旅程提醒了我,全球化带来的相互作用不只是摧毁文化;他们能够创造新的文化,生机,传播存在已久的传统。这不像生态“边缘效应”,它是用来描述两个不同的生态系统相遇发生了什么,例如,森林和草原。在这个接口,那里是最小密度和生命形式的最大的多样性,每种生物都可以从这两个生态系统的核心作画。有时最有趣的事情发生在边缘。在交叉口可以显示意想不到的连接。 4 文化是一个由世界每个角落的礼物组成的织物。发现世界的一种方式是例如通过深入挖掘其传统。例如音乐方面,在任何的大提琴演奏家的曲目的核心是由巴赫大提琴组曲。每个组件的核心是一个称为萨拉班德舞曲的舞蹈动作。这种舞蹈起源于北非的柏柏尔人的音乐,它是一个缓慢的、性感的舞蹈。它后来出现在西班牙,在那里被禁止,因为它被认为是下流的。西班牙人把它带到了美洲,也去了法国,在那里成为一个优雅的舞蹈。在1720年,巴赫公司的萨拉班德在他的大提琴组曲运动。今天,我扮演巴赫,一个巴黎裔美国人的中国血统的音乐家。所以谁真正拥有的萨拉班德?每一种文化都采用了音乐,使其具有特定的内涵,但每一种文化都必须共享所有权:它属于我们所有人。 5 1998年,我从丝绸之路发现在数千年来从地中海和太平洋许多文化间观念的流动。当丝绸之路合奏团执行,我们试图把世界上大部分集中在一个阶段。它的成员是一个名家的同等团体,大师的生活传统是欧洲、阿拉伯、阿塞拜疆、亚美尼亚、波斯、俄罗斯、中亚、印度、蒙古、中国、韩国或日本。他们都慷慨地分享他们的知识,并好奇和渴望学习其他形式的表达。 6 在过去的几年里,我们发现每一个传统都是成功的发明的结果。确保传统的生存的一个最好的方法是由有机进化,目前利用我们所有可用的工具。通过录音和电影;通过驻在博物馆、大学、设计学校和城市;通过表演从教室到体育场,合奏的音乐家,包括我自己,学习有用的技能。回到家中,我们和其他人分享这些技能,确保我们的传统在文化桌上有一席之地。 7 我们发现,在本国执行传统出口的是国外激励从业者。最重要的是,我们对彼此的音乐发展出了激情,并建立了相互尊重、友谊和信任的纽带,每一次我们都在舞台上这都是可触及的。这种欢乐的互动是为了一个理想的共同的更大的目标:我们始终能够通过友好的对话解决任何分歧。我们相互开放,我们形成一个桥进入陌生的传统,驱逐往往伴随着变化和错位的恐惧。换句话说,当我们扩大我们看世界的镜头的时候,我们更好地了解自己,自己的生活和文化。我们与我们的小星球的遥远的行星有更多的共同分享,而不是我们意识到的。 8 发现这些共同的文化是很重要的,但不只是为了艺术的缘故。所以我们的许多城市,不仅是伦敦,纽约,东京,现在即使甚至是中小城市正在经历着移民潮。我们将如何吸取同化有自己独特的习惯的人群?移民不可避免地会导致抵抗和冲突,就像过去一样?有什么关于德国的土耳其人口的阿尔巴尼亚人在意大利,北非人在西班牙和法国?文化繁荣的引擎可以帮助我们找出如何集合可以和平融合,同时不牺牲个性身份。这不是政治正确性。它是关于对人而言什么是珍贵的承认,和每一个文化已经给予我们世界的礼物。

会计专业英语重点1

Unit 1 Financial information about a business is needed by many outsiders .These outsiders include owners, bankers, other creditors, potential investors, labor unions, government agencies ,and the public ,because all these groups have supplied money to the business or have some other interest in the business that will be served by information about its financial position and operating results. 许多企业外部的人士需要有关企业的财务信息,这些外部人员包括所有者、银行家、其他债权人、潜在投资者、工会、政府机构和公众,因为这些群体对企业投入了资金,或享有某些利益,所以必须得到企业财务状况和经营成果信息。 Unit 2 Each proprietorship, partnership, and corporation is a separate entity. 每一独资企业、合伙企业和股份公司都是一个单独的主体。 In accrual accounting, the impact of events on assets and equities is recognized on the accounting records in the time periods when services are rendered or utilized instead of when cash is received or disbursed. That is revenue is recognized as it is earned, and expenses are recognized as they are incurred –not when cash changes hands .if the cash basis accounting were used instead of the accrual basis, revenue and expense recognition would depend solely on the timing of various cash receipts and disbursements. 在权责发生制下,视服务的提供而非现金的收付在本期对资产和权益的影响作出会计记录。即,收入是在赚取时确认,费用是在发生时确认——而不是在现金转手时。如果现金收付制替代权责发生制,那么收入和费用仅仅依靠各种现金收付活动的时间确定来确认。 Unit 3 During each accounting year ,a sequence of accounting procedures called the accounting cycle is completed. 在每一会计年度内,要依次完成被称为会计循环的会计程序。 Transactions are analyzed on the basis of the business documents known as source documents and are recorded in either the general journal or the special journal, i. e . the sales journal ,the purchases journal (invoice register ) ,cash receipts journal and cash disbursements journal . 根据业务凭证即原始凭证分析各项交易,并记入普通日记账或特种日记账,也就是销货日记账,购货日记账(发票登记簿),现金收入日记账和现金支出日记账。 A trial balance is prepared from the account balance in the ledger to prove the equality of debits and credits. 根据分类账户的余额编制试算平衡表,借以验证借项和贷项是否相等。 A T-account has a left-hand side and a right-hand side, called respectively the debit side and credit side. 一个T 型账户有左方和右方,分别称做借方和贷方。 After transactions are entered ,account balance (the difference between the sum of its debits and the sum of its credits ) can be computed.

会计专业英语期末试题 )

期期末测试题 Ⅰ、Translate The Following Terms Into Chinese 、 1、entity concept 主题概念 2、depreciation折旧 3、double entry system 4、inventories 5、stable monetary unit 6、opening balance 7、current asset 8、financial report 9、prepaid expense 10、internal control 11、cash flow statement 12、cash basis 13、tangible fixed asset 14、managerial accounting 15、current liability 16、internal control 17、sales return and allowance 18、financial position 19、balance sheet 20、direct write-off method Ⅱ、Translate The Following Sentences Into Chinese 、 1、Accounting is often described as an information system、It is the system that measures business activities, processes into reports and communicates these findings to decision makers、 2、The primary users of financial information are investors and creditors、Secondary users include the public, government regulatory agencies, employees, customers, suppliers, industry groups, labor unions, other companies, and academic researchers、 3、There are two sources of assets、One is liabilities and the other is owner’s equity、Liabilities are obligations of an entity arising from past transactions or events, the settlement of which may result in the transfer or use of assets or services in the future、 资产有两个来源,一个就是负债,另一个就是所有者权益。负债就是由过去得交易或事件产生得实体得义务,其结算可能导致未来资产或服务得转让或使用。 4、Accounting elements are basic classification of accounting practices、They are essential units to present the financial position and operating result of an entity、In China, we have six groups of accounting elements、They are assets, liabilities, owner’s equity, revenue, expense and profit (income)、会计要素就是会计实践得基础分类。它们就是保护财务状况与实体经营

学术英语课后翻译答案

学术英语(理工)课后英译汉练习答案 Text 1 1有些人声称黑客是那些扩宽知识界限而不造成危害的好人(或即使造成危害,但并非故意而为),而“破碎者”才是真正的坏人。 2这可以指获取计算机系统的存储内容,获得一个系统的处理能力,或捕获系统之间正在交流的信息。 3那些系统开发者或操作者所忽视的不为人知的漏洞很可能是由于糟糕的设计造成的,也可能是为了让系统具备一些必要的功能而导致计划外的结果。 4另一种是预先设定好程序对特定易受攻击对象进行攻击,然而,这种攻击是以鸟枪式的方式发出的,没有任何具体目标,目的是攻击到尽可能多的潜在目标。 5另外,考虑安装一个硬件防火墙并将从互联网中流入和流出的数据限定在仅有的几个你真正需要的端口,如电子邮件和网站流量。 Text 2 1看似无害的编程错误可以被利用,导致电脑被侵入并为电脑蠕虫和病毒的繁衍提供温床。 2当一个软件漏洞被发现,黑客可以将漏洞变成一个侵入点,从而造成极大的破坏,在这之前,往往需要争分夺秒地利用正确的软件补丁来防止破坏的发生。 3最简单的钓鱼骗局试图利用迅速致富的伎俩诱使诈骗目标寄钱。但网络骗子们也变得越来越狡猾,最近的陷阱是通过发送客户服务的电子邮件让用户进入假银行或商 业网站,并在那里请他们“重新输入”他们的账户信息。 4间谍软件与垃圾邮件和钓鱼网络一起,构成了三个令人生厌的互联网害虫。尽管有些程序可以通过入侵软件漏洞从而进入电脑,但这些有害而秘密的程序通常会随着 其他通常是免费的应用软件侵入到计算机系统中。 5尽管因特网已经彻底改变了全球通讯,但是对于那些意图为了罪恶目的而利用网络力量的人和那些负责阻止这些网络犯罪的人来说,他们之间的较量才刚刚开始。Text 5 1.最近在《纽约时报》上刊登的一篇文章谈到了一种新计算机软件,该软件在瞬间就能通 过数以千计的法律文件筛选并寻找到那些可诉讼的条款,这为律师们节省了在阅读文件上所花费的数百小时。 2.他们主要靠耕种来养活自己,然后再多种一些用以物品交易或卖一些盈余 3.从事农业和畜牧业者的绝对数量大约在1910年时达到顶峰(约有1,100—1,200万), 在此之后人数便急剧下降 4.这个故事总结了美国几个世纪以来的工作经历,从失业工人的层面上讲是悲剧,但从全 国劳动力的层面上讲是件好事。 5.人工智能是一种新的自动化技术吗?是一种削弱了曾经是20世纪末就业标志的脑力工 作的技术吗?是一种只会消除更好的工作机会的技术吗? Text 6 1.就前者来说,玩家按照顺序移动,(那么)每个人都了解其他玩家之前的动作。就 后者而言,玩家同时做出动作,则不了解其他玩家的动作。 2.当一个人思考别人会如何反应的时候,他必须站在别人的角度,用和他们一样的思 考方式进行思考一个人不能将自己的推理强加在别人的身上。 3.尽管各位玩家同时做出动作,不知道其他玩家当前的动作,然而,每个玩家都必须

会计专业英语翻译

. 1. Accounting first is an economic calculation. Economic calculation includes both static phenomenon on the economy's stock of the situation, including the situation of the period of dynamic flow, including both pre-calculated plan, but also after the actual calculation. Accounting is a typical example of economic calculation, calculation of economic calculation in addition to accounting, which includes statistical computing and business computing. 2. Accounting is an economic information systems. It would be a company dispersed into the business activities of a group of objective data, providing the company's performance, problems, and enterprise funds, labor, ownership, income, costs, profits, debt, and other information. Clearly, the accounting is to provide financial information-based economy information systems, business is the licensing of a points, thus accounting has been called "corporate language." 3. Accounting is an economic management.The accounting is social production develops to a certain stage of the product development and production is to meet the needs of the management, especially with the development of the commodity economy and the emergence of competition in the market through demand management on the economy activities strict control and supervision. At the same time, the content and form of accounting constantly improve and change, from a purely accounting, scores, mainly for accounting operations, external submit accounting statements, as in prior operating forecasts, decision-making, on the matter of economic activities control and supervision, in hindsight, check. Clearly, accounting whether past, present or future, it is people's economic management activities.

会计英语翻译

A business that is owned and controlled by one person is considered to be a sole trader. This form of business ownership is simple and generally inexpensive. The owner of a sole trader is entitled to make all the decisions in the organization and retain all the profits. A partnership is an organization where two or more person (partners) own and control a business. In a partnership, it is normal for each partner to have unlimited liability for debits of the business. In addition, partnerships have a limited life, and can be dissolved on the death or retirement of a partner. A corporation is a business that is organized as a separate legal entity under the law. Corporations are owned by shareholders who contribute to the capital of the business by buying shares in the corporation. The shareholders are not personally liable for(对……有责任) the debits of the corporation. In most corporations, control of the affairs of the corporation is maintained by a board of directors who are elected by shareholders. A business that is owned and controlled by one person is considered to be a sole trader. This form of business ownership is simple and generally inexpensive.一人拥有和控制的企业被称为个人独资企业。这种企业形式比较简单,而且通常投资额较小。The owner of a sole trader is entitled to make all the decisions in the organization and retain all the profits.个人独资企业的所有者对企业内所有的事务制定决策并拥有企业的全部利润。A partnership is an organization where two or more person (partners) own and control a business. In a partnership, it is normal for each partner to have unlimited liability for debits of the business. In addition, partnerships have a limited life, and can be dissolved on the death or retirement of a partner.合伙企业是由两个或以上的人(合伙人)共同拥有和控制的企业组织形式。一般在合伙企业中,每个合伙人对企业债务都承担无限责任。同时,合伙企业的寿命也是有限的,企业可能因为某个合伙人死亡或退休而终止。 A corporation is a business that is organized as a separate legal entity under the law.公司是依照法律规定成立的独立法人组织。Corporations are owned by shareholders who contribute to the capital of the business by buying shares in the corporation. 公司由股东拥有,股东通过购买公司的股份为公司提供资本。The shareholders are not personally liable for the debits of the corporation. In most corporations, control of the affairs of the corporation is maintained by a board of directors who are elected by shareholders. 股东个人对公司的债务不承担无限责任。大多数公司的经营业务由股东选出的董事会实施控制。

学术英语Unit1~4课文翻译

Unit 1 Text A 神经过载与千头万绪的医生 患者经常抱怨自己的医生不会聆听他们的诉说。虽然可能会有那么几个医生确实充耳不闻,但是大多数医生通情达理,还是能够感同身受的人。我就纳闷为什么即使这些医生似乎成为批评的牺牲品。我常常想这个问题的成因是不是就是医生所受的神经过载。有时我感觉像变戏法,大脑千头万绪,事无巨细,不能挂一漏万。如果病人冷不丁提个要求,即使所提要求十分中肯,也会让我那内心脆弱的平衡乱作一团,就像井然有序同时演出三台节目的大马戏场突然间崩塌了一样。有一天,我算过一次常规就诊过程中我脑子里有多少想法在翻腾,试图据此弄清楚为了完满完成一项工作,一个医生的脑海机灵转动,需要处理多少个细节。 奥索里奥夫人 56 岁,是我的病人。她有点超重。她的糖尿病和高血压一直控制良好,恰到好处。她的胆固醇偏高,但并没有服用任何药物。她锻炼不够多,最后一次 DEXA 骨密度检测显示她的骨质变得有点疏松。尽管她一直没有爽约,按时看病,并能按时做血液化验,但是她形容自己的生活还有压力。总的说来,她健康良好,在医疗实践中很可能被描述为一个普通患者,并非过于复杂。 以下是整个 20 分钟看病的过程中我脑海中闪过的念头。 她做了血液化验,这是好事。 血糖好点了。胆固醇不是很好。可能需要考虑开始服用他汀类药物。 她的肝酶正常吗? 她的体重有点增加。我需要和她谈谈每天吃五种蔬果、每天步行 30 分钟的事。 糖尿病:她早上的血糖水平和晚上的比对结果如何?她最近是否和营 养师谈过?她是否看过眼科医生?足科医生呢? 她的血压还好,但不是很好。我是不是应该再加一种降血压的药?药 片多了是否让她困惑?更好地控制血压的益处和她可能什么药都不吃 带来的风险孰重孰轻?

(完整版)会计专业英语重点词汇大全

?accounting 会计、会计学 ?account 账户 ?account for / as 核算 ?certified public accountant / CPA 注册会计师?chief financial officer 财务总监?budgeting 预算 ?auditing 审计 ?agency 机构 ?fair value 公允价值 ?historical cost 历史成本?replacement cost 重置成本?reimbursement 偿还、补偿?executive 行政部门、行政人员?measure 计量 ?tax returns 纳税申报表 ?tax exempt 免税 ?director 懂事长 ?board of director 董事会 ?ethics of accounting 会计职业道德?integrity 诚信 ?competence 能力 ?business transaction 经济交易?account payee 转账支票?accounting data 会计数据、信息?accounting equation 会计等式?account title 会计科目 ?assets 资产 ?liabilities 负债 ?owners’ equity 所有者权益 ?revenue 收入 ?income 收益

?gains 利得 ?abnormal loss 非常损失 ?bookkeeping 账簿、簿记 ?double-entry system 复式记账法 ?tax bearer 纳税人 ?custom duties 关税 ?consumption tax 消费税 ?service fees earned 服务性收入 ?value added tax / VAT 增值税?enterprise income tax 企业所得税?individual income tax 个人所得税?withdrawal / withdrew 提款、撤资?balance 余额 ?mortgage 抵押 ?incur 产生、招致 ?apportion 分配、分摊 ?accounting cycle会计循环、会计周期?entry分录、记录 ?trial balance试算平衡?worksheet 工作草表、工作底稿?post reference / post .ref过账依据、过账参考?debit 借、借方 ?credit 贷、贷方、信用 ?summary/ explanation 摘要?insurance 保险 ?premium policy 保险单 ?current assets 流动资产 ?long-term assets 长期资产 ?property 财产、物资 ?cash / currency 货币资金、现金

会计方面专业术语的英文翻译

会计方面专业术语的xx acceptance承兑 account账户 accountant会计员 accounting会计 accounting system会计制度 accounts payable应付账款 accounts receivable应收账款 accumulated profits累积利益 adjusting entry调整记录 adjustment调整 administration expense管理费用 advances预付 advertising expense广告费 agency代理 agent代理人 agreementxx allotments分配数 allowance津贴 amalgamation合并 amortization摊销

amortized cost应摊成本 annuities年金 applied cost已分配成本 applied expense已分配费用 applied manufacturing expense己分配制造费用apportioned charge摊派费用 appreciation涨价 article of association公司章程 assessment课税 assets资产 attorney fee律师费 audit审计 auditor审计员 average平均数 average cost平均成本 bad debt坏账 balance余额 balance sheet资产负债表 bank account银行账户 bank balance银行结存 bank charge银行手续费

bank deposit银行存款 bank discount银行贴现bank draft银行汇票 bank loan银行借款 bank overdraft银行透支bankers acceptance银行承兑bankruptcy破产 bearer持票人 beneficiary受益人 bequest遗产 bill票据 bill of exchange汇票 bill of lading提单 bills discounted贴现票据bills payable应付票据 bills receivable应收票据board of directors董事会bonds债券 bonus红利 book value账面价值bookkeeper簿记员

会计专业英语期末考试练习卷(new)

会计专业英语期末考试练习卷(new)

1. The economic resources of a business are called : B A. Owner ’s Equity B. Assets C. Accounting equation D. Liabilities 2. DTK Company has a $3500 accounts receivable from GRS Company. On January 20, GRS Company makes a partial payment of $210 0 to DTK Company. The journal entry made on January 20 by DTK Company to record this transaction includes: D A. A debit to the cash receivable account of $2100. B. A credit to the accounts receivable account of $2100. C. A debit to the cash account of $1400. D. A debit to the accounts receivable account of $1400. 3. In general terms, financial assets appear in the balance sheet at: A A. Face value. 账面价值 B. Current value. 现值 C. Market value. 市场价值 D. Estimated future sales value. 4. Each of the following measures strengthens intern al control over cash receipts except : D A. The use of a voucher system. B. Preparation of a daily listing of all checks received through the mail. C. The deposit of cash receipts intact in the bank on a daily basis. D. The use of cash registers. 5. Which of the following items is the greatest in dollar amount? D A. Beginning inventory B. Cost of goods sold. C. Cost of goods available for sale D. Ending inventory 6. Why do companies prefer the LIFO inventory 后进先出法method during a period of rising prices? B A. Higher reported income B. Lower income taxes C. Lower reported income D. Higher ending inventory 7. Which of the following characteristics would prevent an item from being included in the classification of plant and equipment? D A. Intangible

研究生学术英语课后习题答案

Unit 1英译汉:15 Outlines are essential to effective speeches.By outlining, you make sure that related ideas are together, that your thoughts flow from one to another, and that the structure of your speech is coherent. You will probably use two kinds of outlines for your speeches--the detailed preparation outline and the brief speaking outline. 发言提纲是有效发言的基础。通过写发言提纲,你可以确保你的想法是关联的,你的思路从一点谈到另一点,你的讲话结构是连贯的,通常准备演讲你可以采用两种提纲方式:详细准备提纲和简单发言提纲。 In a preparation outline, you should state your specific purpose and central idea, and identify main points and sub--points using a consistent pattern. The speaking outline sho uld consist of brief notes to help you while you deliver the speech. It should contain ke y words or phrases to bolster your memory. In making up your speaking outline, follow the same visual framework used in your preparation outline. Keep the speaking outline a s brief as possible and be sure it is plainly legible 在准备提纲中,应该写出你的特定目的及中心思想,并以连贯的方式确定主要观点和次要观点。发言提纲应该由简要的提要组成,这些提要在你讲话时能够给你一些帮助。发言提纲还应包括帮助你记忆的重点词或重点短语。在写发言提纲时,可采用准备提纲的模式,尽可能使你的发言提纲简要,同时,要确保提纲清晰、易于辨认。 汉译英: 当你发表学术演讲时,首先要做好充分的准备;其次,你演讲的主要观点要明确,层次要清楚。演讲时,语速不要过快,语言要清晰。不要总是在读你准备好的稿子。最后,你应该经常看一下你的听众。这样,一方面你对你的听众表示尊重,另一方面,你可以更顺利地进行你的演讲。 Before you deliver an academic speech, firstly you should get well prepared for it. Then, you should make your major points clear in your speech, and your speech should be well organized. When speaking, you should not speak too fast, and your language should be explicit. Don’t always read the notes you prepared beforehand. From time to time, you should look at your audience. On one hand, you can show your respect to your audience, and on the other hand, you will be able to go on with your speech more smoothly.

会计英语中英文对照

会计方面专业术语的英文翻译 acceptance 承兑 account 账户 accountant 会计员 accounting 会计 accounting system 会计制度 accounts payable 应付账款 accounts receivable 应收账款 accumulated profits 累积利益 adjusting entry 调整记录 adjustment 调整 administration expense 管理费用 advances 预付 advertising expense 广告费 agency 代理 agent 代理人 agreement 契约 allotments 分配数 allowance 津贴 amalgamation 合并 amortization 摊销 amortized cost 应摊成本 annuities 年金 applied cost 已分配成本 applied expense 已分配费用 applied manufacturing expense 己分配制造费用apportioned charge 摊派费用 appreciation 涨价 article of association 公司章程 assessment 课税 assets 资产 attorney fee 律师费 audit 审计 auditor 审计员 average 平均数 average cost 平均成本 bad debt 坏账 balance 余额

balance sheet 资产负债表 bank account 银行账户 bank balance 银行结存 bank charge 银行手续费 bank deposit 银行存款 bank discount 银行贴现 bank draft 银行汇票 bank loan 银行借款 bank overdraft 银行透支 bankers acceptance 银行承兑 bankruptcy 破产 bearer 持票人 beneficiary 受益人 bequest 遗产 bill 票据 bill of exchange 汇票 bill of lading 提单 bills discounted 贴现票据 bills payable 应付票据 bills receivable 应收票据 board of directors 董事会 bonds 债券 bonus 红利 book value 账面价值 bookkeeper 簿记员 bookkeeping 簿记 branch office general ledger 支店往来账户broker 经纪人 brought down 接前 brought forward 接上页 budget 预算 by-product 副产品 by-product sales 副产品销售 capital 股本 capital income 资本收益 capital outlay 资本支出 capital stock 股本 capital stock certificate 股票 carried down 移后 carried forward 移下页 cash 现金 cash account 现金账户 cash in bank 存银行现金 cash on delivery 交货收款

相关文档

- 会计专业英语词汇大全[1]

- 考研会计专业英语试题

- 会计专业英语期末试题期期末测试题

- 《财会专业英语》期末试卷及答案

- 财务会计英语专业词汇大全.

- 会计专业英语期末复习资料

- 会计专业英语期末试题 )

- (完整版)会计专业英语词汇大全

- 会计专业英语期末考试练习卷new)

- 会计专业英语期末试题 )

- 会计专业英语期末试题 )

- 会计专业英语期末试题 )知识讲解

- 《财会专业英语》期末试卷及答案

- 《会计专业英语》期末复习资料

- 会计专业英语重要词汇(完成)

- [南开大学]《会计专业英语》19秋期末考核(答案参考)

- 《财会专业英语》期末试卷及答案

- 中国地质大学(北京)《会计专业英语》期末考试拓展学习(七)

- 会计专业英语期末试题 )

- 会计专业英语期末考试练习卷(new)