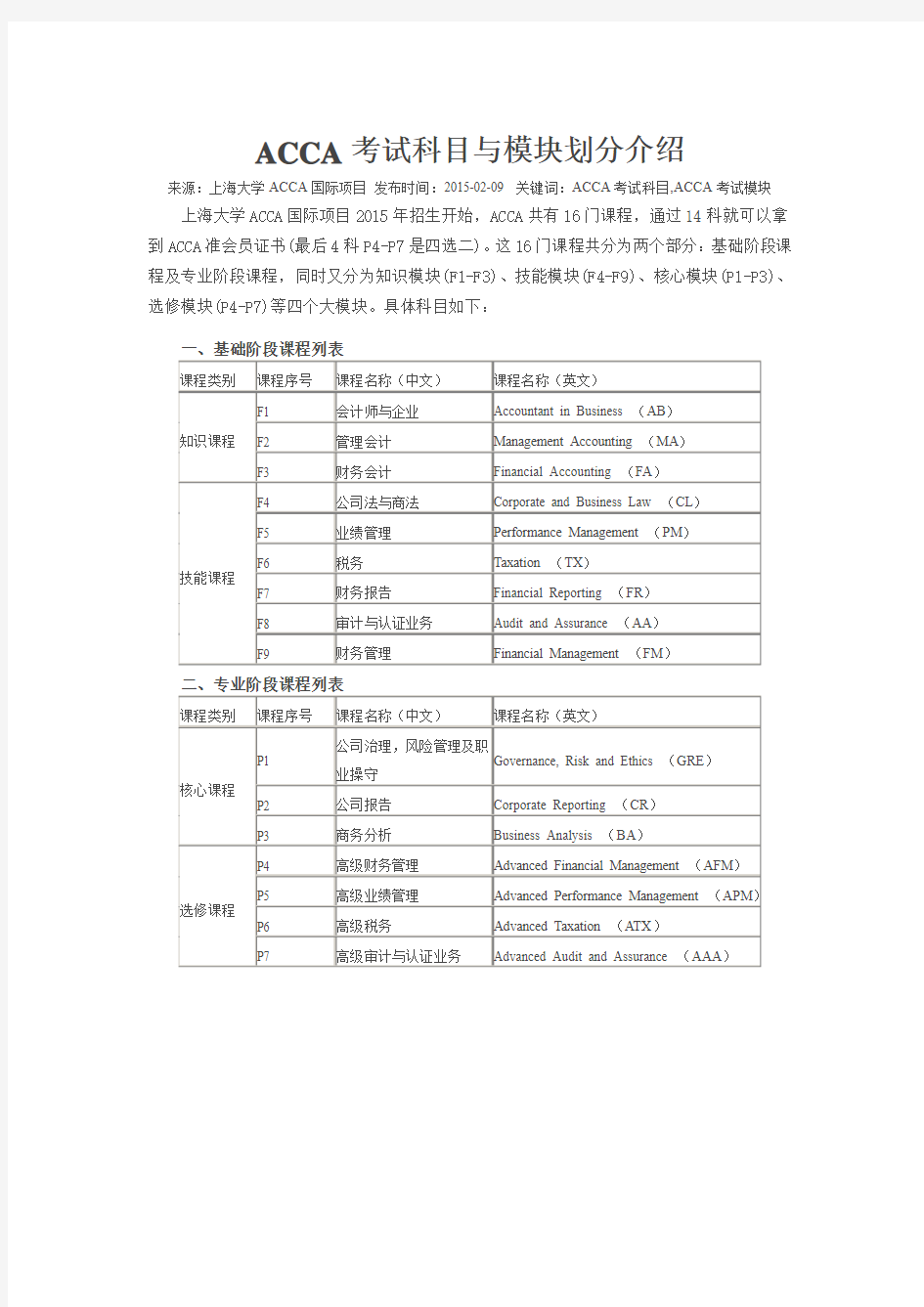

ACCA考试科目与模块划分介绍

ACCA考试审计科目模拟测试(4)

ACCA考试审计科目模拟测试(4) 本文由高顿ACCA整理发布,转载请注明出处 Financial Management 1 (a) Weighted average cost of capital (WACC) calculation Cost of equity of KFP Co = 4·0 + (1·2 x (10·5 – 4·0)) = 4·0 + 7·8 = 11·8% using the capital asset pricing model To calculate the after-tax cost of debt, linear interpolation is needed After-tax interest payment = 100 x 0·07 x (1 – 0·3) = $4·90 Year Cash flow $ 10% discount PV ($) 5% discount PV ($) 0 Market value (94·74) 1·000 (94·74) 1·000 (94·74) 1 to 7 Interest 4·9 4·868 23·85 5·786 28·35 7 Redemption 100 0·513 51·30 0·711 71·10 –––––––––– (19·59) 4·71 –––––––––– After-tax cost of debt = 5 + ((10 – 5) x 4·71)/(4·71 + 19·59) = 5 + 1·0 = 6·0% Number of shares issued by KFP Co = $15m/0·5 = 30 million shares Market value of equity = 30m x 4·2 = $126 million Market value of bonds issued by KFP Co = 15m x 94·74/100 = $14·211 million

2018年ACCA F3考试题型介绍

中公财经培训网:https://www.sodocs.net/doc/d312999540.html,/对于很多已经报名参加6月份ACCA考试的小伙伴来说,F3阶段的考试考哪些题型的确是大家需要认真了解一下的。中公财经小编就F3阶段考试题型给大家整理了一下,具体情况如下所示; Section A will contain 35 two mark objective questions. Section B will contain 2 fifteen mark multi-task questions. One will test consolidations and the other will test accounts preparation. 对于9月马上推出的ACCA F阶段全机考,我们也对题型做了解读: 9月份ACCA 机考CBEs题型介绍 (一)客观题(Objective test questions/ OT questions)客观题是指这些单一的,题干较短的,并且自动判分的题目。每道客观题的分值为2分,考生必须回答的完全正确才可以得分,即使回答正确一部分,也不能得到分数。 (二)案例客观题(OT case questions) 案例客观题是ACCA引入的新题型,每道案例客观题都是由一组与一个案例相关的客观题组成的,因此要求考生从多个角度来思考一个案例。这种题型能很好的反映出考生将如何在实践中完成这些任务。案例客观题会出现在2016年9月份的笔试中,这意味着CBEs考试和笔试的格式在本次考试中将完全一致。 (三) 主观题(Constructed response questions/ CR qustions)考生将使用电子表格程序和文字处理程序去完成主观题的回答。就像笔试中的主观题一样,答案最终将由专家判分。 这些变化都是更紧密地反映了考生在工作场所中执行同样任务的方式,所以考生必须具备现代金融专业所需要的最相关的技能。 考试前或是备考时,先了解一下考试题型是非常有必要的。中公财经小编在这里预祝大家在接下来的考试中,过过过。。。

对于ACCA考试科目中F8的题型分析

对于ACCA考试科目中F8的题型分析 关于ACCA考试科目中,各科都考哪些题型呢?中公财经网小编就以F8为例给大家简单介绍一 下吧。 (一)客观题(Objective test questions/OT questions)客观题是指这些单一的,题干较短的,并且自动判分的题目。每道客观题的分值为2分,考生必须回答的完全正确才可以得分,即使回答正确 一部分,也不能得到分数。 (二)案例客观题(OT case questions) 案例客观题是ACCA引入的新题型,每道案例客观题都是由一组与一个案例相关的客观题组成的,因此要求考生从多个角度来思考一个案例。这种题型能很好的反映出考生将如何在实践中完成这些任务。案例客观题会出现在2016年9月份的笔试中,这意味着CBEs考试和笔试的格式在本次考试中将完全一致。 (三)主观题(Constructed response questions/CR qustions)考生将使用电子表格程序和文字处理程序去完成主观题的回答。就像笔试中的主观题一样,答案最终将由专家判分。 今天就奉上同学回忆出的12月ACCA F8科目考试真题,勇敢的童鞋赶紧来测试一下,你到底能否考过F8吧! Section A部分真题 第一道案例选择题印象比较深,是关于professional ethical,考了fundamental professional ethical和threat。 第二道是关于payroll system,考了audit procedure,completeness,understatement test,其中还有一道计算payroll expense。 第三道问了audit opinion,还有SP,有overstatement test。 Section B部分真题 第一道大题,有16分的audit risk(identify and response)找出8个,factors to

ACCA考试会计模拟习题(13)

ACCA考试会计模拟习题(13) 本文由高顿ACCA整理发布,转载请注明出处 3 Mary Hobbes joined the board of Rosh and Company,a large retailer,as finance director earlier this year. Whilst she was glad to have finally been given the chance to become finance director after several years as a financial accountant,she also quickly realised that the new appointment would offer her a lot of challenges. In the first board meeting,she realised that not only was she the only woman but she was also the youngest by many years. Rosh was established almost 100 years ago. Members of the Rosh family have occupied senior board positions since the outset and even after the company’s flotation 20 years ago a member of the Rosh family has either been executive chairman or chief executive. The current longstanding chairman,Timothy Rosh,has already prepared his slightly younger brother,Geoffrey (also a longstanding member of the board)to succeed him in two years’time when he plans to retire. The Rosh family,who still own 40% of the shares,consider it their right to occupy the most senior positions in the company so have never been very active in external recruitment. They only appointed Mary because they felt they needed a qualified accountant on the board to deal with changes in international financial reporting standards. Several former executive members have been recruited as non-executives immediately after they retired from full-time service. A recent death,however,has reduced the number of non-executive directors to two. These sit alongside an executive board of seven that,apart from Mary,have all been in post for over ten years. 更多ACCA资讯请关注高顿ACCA官网:https://www.sodocs.net/doc/d312999540.html,

ACCA考试会计师与企业(基础阶段)历年真题精选及详细解析1110-74

ACCA考试会计师与企业(基础阶段)历年真题精选及详细解析1110-74 1. A company rents its factory for $90,000 per annum. This year 60,000 units have been manufactured in the factory utilising 75% of its total capacity. Next year the plan is to manufacture 100,000 units by using the existing factory at full capacity and by renting just sufficient additional capacity. The additional capacity is available at the same rental cost per square metre as the existing factory. What is the budgeted total rental cost for next year? $() 12.答案:$112,500 The company produces 60,000 units at 75% capacity. Therefore it would produce 80,000 units at 100% capacity (60,000 1 0.75). Rent per unit of output at 100% capacity = $1.125 (90,000 1 1

最新最全ACCA中F5大纲考试科目介绍

最新最全ACCA中F5大纲考试科目介绍 本文由高顿ACCA整理发布,转载请注明出处 Performance Management (F5) 科目介绍: F5《业绩管理》是F2《管理会计》的后续课程,它也帮助考生建立了P5《高级业绩管理》的学习基础。 大纲首先介绍了更多的与业管理会计的内容,这些内容是F2(管理会计)已经涉及的,主要是关于成本费用的处理。这里复习的目的是使得考生在学习F5 这门课程时对管理会计技能上有着更深的了解。 大纲然后涉及决策问题。学员需要解决资源短缺、定价和自制或外部购买等问题,还需要了解这些和业绩评估有何关联。风险和不确定性是真实生活中的一个因素,考生必须了解风险并且能够运用一些基础的方法来解决存在二决策内部的固有风险。

预算是很多会计师职业生涯中很重要的一部分。大纲阐述了不同的预算方法以及它们存在的问题。对会计师来说预算的行为方面的理解是很重要的。大纲包括个人对预算做出反应的方式。 接下来是标准成本法和差异。在F2 中涉及的所有差异计算是学习F5 的基础是必须掌握的。除此之外,新增加了混合差异和收益差异不计划差异和经营差异两大类。对二会计师来说要理解这些计算出来的数字并且明白在绩效背景下有着什么意义。 大纲还包括业绩评估和控制。这是大纲主要的一个部分。会计师需要理解一项业务应该如何管理和控制。会计师应该对管理上的财务和非财务业绩评估的重要性做出正确的评价。会计师也应该鉴别在评估事业部制公司的业绩中存在的困难和因为未能考虑外部环境对业绩的影响而导致的问题。这些内容直接和P5(高级业绩管理)相关。 近几年考试通过率趋势图: 知识结构:

2018年ACCA F5-F5考试各科目题量及分值

2018年ACCA F5-F5考试各科目题量及分值 2018年ACCA F5-F9考试新的政策出炉,广东中公金融人为广大考生整理发布广东省各大银行校园招聘信息,及时获知当前广东银行招聘信息,可及时关注2017银行校园招聘公告汇总。 2018年ACCA F5-F9考试将全面执行机考形式,对于机考的科目也进行了调整,从中F5-F9考题各科目的数量与分值变化如下: 科目一:F5 Performance Management Section A 客观题,共15题,每题2分,共30分 Section B 案例题,共3个案例,每个案例包含5道客观题,每题2分,共30分 Section C 主观题,共2道主观题,每题20分,共计40分 科目二:F6 Taxation Section A 客观题,共15题,每题2分,共30分 Section B 案例题,共3个案例,每个案例包含5道客观题,每题2分,共30分 Section C 主观题,共3道主观题,1题10分,2题15分,共计40分 科目三:F7 Financial Reporting Section B 案例题,共3个案例,每个案例包含5道客观题,每题2分,共30分 Section C 主观题,共2道主观题,每题20分,共计40分 科目四:F8 Audit and Assurance F8的考试题型分为2个Section: Section A 案例题,共3个案例,每个案例包含5道客观题,每题2分,共30分 Section B 主观题,1个30分的主观题 + 2个20分的主观题 科目五:F9 Financial Management Section A 客观题,共15题,每题2分,共30分

2015年6月ACCA考试《财务报告(International)》真题及详解

2015年6月ACCA考试《财务报告(International)》真题 (总分:100.00,做题时间:180分钟) 一、Section A – ALL 20 questions are compulsory and MUST be attempted (总题数:20,分数:40.00) 1.Faithful representation is a fundamental characteristic of useful information within the IASB’s Conceptual framework for financial reporting. Which of the following accounting treatments correctly applies the principle of faithful representation? (分数:2.00) A.Reporting a transaction based on its legal status rather than its economic substance B.Excluding a subsidiary from consolidation because its activities are not compatible with those of the rest of the group C.Recording the whole of the net proceeds from the issue of a loan note which is potentially convertible to equity shares as debt (liability) D.Allocating part of the sales proceeds of a motor vehicle to interest received even though it was sold with 0%(interest free) finance √ 解析:The substance is that there is no ‘free’ finance; its cost, as such, is built into the selling price. 2.Which of the following statements relating to intangible assets is true? (分数:2.00) A.All intangible assets must be carried at amortised cost or at an impaired amount; they cannot be revaluedupwards B.The development of a new process which is notexpected to increase sales revenues may still be recognised asan intangible asset √ C.Expenditure on the prototype of a new engine cannot be classified as an intangible asset because the prototypehas been assembled and has physical substance D.Impairment losses for a cash generating unit are first applied to goodwill and then to other intangible assets beforebeing applied to tangible assets 解析:A new process may produce benefits (and therefore be recognised as an asset) other than increased revenues, e.g. it may reduce costs. 3.Each of the following events occurred after the reporting date of 31 March 2015, but before the financial statementswere authorised for issue.

acca一共要考几门课

acca一共要考几门课 ACCA一共15门课程共分为两个阶段,分别是F阶段和P阶段,其中又分为几个部分,F1-F3属于知识课程部分,F4-F9属于技能课程部分,SBL-SBR属于核心课程部分,P4-P7(选修两门)属于选修课程部分。考生只需通过13门考试即可。 考试的具体课程: 基础阶段课程: 知识课程(共3门) F1 Accountant in Business商业会计 F2 Management Accounting管理会计 F3 Financial Accounting财务会计 技能课程(共6门) F4 Corporate and Business Law(CHN)公司法与商法 F5 Performance Management业绩管理 F6 Taxation(CHN)税法 F7 Financial Reporting财务报告 F8 Audit and Assurance审计与认证 F9 Financial Management财务管理 专业阶段:核心课程 SBL战略商业领袖Strategic Business Leader SBL战略商业报告Strategic Business Reporting 选修课程(任选其中2门) P4 Advanced Financial Management高级财务管理 P5 Advanced Performance Management高级业绩管理 P6 Advanced Taxation高级税法 P7 Advanced Audit and Assurance高级审计和认证

急速通关计划 ACCA全球私播课大学生雇主直通车计划周末面授班寒暑假冲刺班其他课程

ACCA各科目全球最高分一览表

ACCA各科目全球最高分一览表 本文由高顿ACCA整理发布,转载请注明出处 提到ACCA大家都觉得十分高端大气上档次,很多科目能考过就已经让周围的小伙伴们惊呆了,但是,看一看ACCA相应科目考试的全球最高分吧,真的是“人外有人,天外有天”,“高手高手高高手”啊! Congratulationsto all the winners of the June 2014 ACCA Genius Hunt Competition! Below is the list of winners of the Genius Hunt Competition! Becker Professional Education are awarding the students with the highest mark in each ACCA paper, a FREE Interactive eBook for a paper of their choice for the December 2014 exams (worth 99 GBP). *we have already received mark confirmation All the winners has been sent anemail with the instructions on how to collect their prizes. 以上这些是今年六月份每个ACCA考试科目全球分数最高的学员获奖名单,ACCA也能考一百分真学霸!! 更多ACCA资讯请关注高顿ACCA官网:https://www.sodocs.net/doc/d312999540.html,

ACCA考试科目F1-F4考试题型及考试重点

ACCA机考F1-F4考试题型及考试重点 ACCA考试Fundamental level F阶段最开始的考试科目F1-F4就是机考科目,2018年3月以后,ACCA考试科目F5-F9也将全面进入机考时代。当然,如果你已经免考ACCA F阶段了,这篇文章就可以略过了,But,如果你还需要跟ACCA F阶段继续周旋和鏖战,那么,以下内容,你要仔细看喽! ACCA考试科目F1-F4的考试内容分为2大模块,Section A &Section B, Section A以单选,多选和判断题为主要类型的题目。每题1-2分,这个部分的题目,单选判断不必说,对则得分,错则不得分。多选题则有统一标准,全对才得分,如果出现任一单一选项错误,也不得分。所以,在做这类题目时,知识点掌握全面扎实才是得分王道! Section B 里面以多任务题为主,什么叫多任务题?题目会引入较长的案例分析,还有图表需要理解分析,题目会以单选或者多选的形式出现,这里的单选选项会超过4个,增加了选择难度,而这个部分的多选,如果能够选对部分选项也能够拿到部分分数,而不会像Section A里面的多选题卡分卡的那么严格。 以上2段内容讲述清楚了题目模块和题目类型,下面我们一起来看一下F1-F4题目分值分布: F1 / FAB Section A (总计76分):46道题,每道题1分或2分 Section B (总计24分):6道多任务题MTQs,每道题4分 F2 / FMA Section A (总计70分):35道题,每道题2分 Section B (总计30分):3道多任务题,每道题10分 F3 / FFA Section A (总计70分):35道题,每道题2分 Section B (总计30分):2道多任务题,每道题15分 F4 Section A (总计70分):45道客观题,其中20道题每题1分;25道题每题2分Section B (总计30分):5道多任务题,每道题6分 考试开始前,监考人员会宣读考场纪律;考生需要在电脑上输入个人信息,监考人员会核对

ACCA F1-F3模拟题及解析(1)

第1章 ACCA F1-F3模拟题及解析(1) 1. Which of the followings belongs to UK Equal Opportunity legislation? i) Disable person 1944 & 1958 ii) Equal pay Act iii)Rehabilitation of offender Act iv)Health and Safety at work 1974 v) Employment Act 2002 A. i) ii) iii) v) B. i) iii) iv) C. i) ii) iii) iv) D. All above 2.A combination of unacceptably high unemployment and unacceptably high inflation is call________. Which one of followings can complete the sentence? A. Inflation B. Deflation C. Depression D. Stagflation 3. Which one of the followings is NOT the suitable solution for clearing with balance of payment deficit? A.Depreciation of currency B. Import quotas and tariff C.Reduce to domestic demand D. Increase to domestic demand 4. Inflation can have negative effect on macro-economic. A. True B. False 5. Fiscal economic policy refer to government use___; ___to influence the aggregate demand .Monetary policy refer to government use___; ___; ___to influence the aggregate demand. A. Taxation, Government spending, Exchange rate, Money supply. Interest rate B. Money supply, Interest rate, Taxation, Government spending, Exchange rate. C. Exchange rate, Interest rate, Government spending, Money supply, Taxation D. Government spending, Money supply, Interest rate, Exchange rate, Taxation 6. Which one of followings is NOT a main accounting function in an organization? A.Financial accounting for external reporting purposes. B.Internal audit function for checking the control system C.Management accounting and cost accounting. D.Financial management for fund rising and investment appraisal. 7. Which one of followings is NOT the purpose of the internal control system? A.Safeguard assets prevent and detect frauds and errors. B.To provide the timely and accurate management information for effective operation of company. C.To make sure company will going concern forever. D.To make sure the quality of financial statement for external reporting purposes. 8. Which one of following is NOT the computer input control? A.Pre-list B.Control total C.Post-list D.Hush total

2018ACCA考试时间和科目

2018年ACCA考试时间和科目汇总 ACCA一年有四次考试,分别在3月、6月、9月、12月,那么具体的ACCA考试时间和科目安排是什么呢,中公小编带大家梳理一遍。 2018年ACCA3月份考试时间安排: 2018.03.05 周一:F8、P7 2018.03.06 周二:F7、P2 2018.03.07 周三:F5、P1、P5 2018.03.08 周四:F6、P3、P6 2018.03.09 周五:F9、P4 2018年3月ACCA考试成绩公布日期:2018年04月16日 2018年ACCA6月份考试时间安排: 2018.06.04 周一:F8、P7 2018.06.05 周二:F7、P2 2018.06.06 周三:F5、P1、P5 2018.06.07 周四:F6、P3、P6 2018.06.08 周五:F9、P4 2018年6月ACCA考试成绩公布日期:2018年07月16日 2018年ACCA9月份考试时间安排: 2018.09.03 周一:Audit and Assurance、Advanced Audit and Assurance 2018.09.04 周二:Taxation、Advanced Taxation、Strategic Business Leader 2018.09.05 周三:Performance Management、Advanced Performance Management 2018.09.06 周四:Financial Reporting、Strategic Business Reporting 2018.09.07 周五:Financial Management、Advanced Financial Management、Corporate and Business Law 2018年9月ACCA考试成绩公布日期:2018年10月16日 2018年ACCA12月份考试时间安排

ACCA考试练习册题目 F2 2012

1、Accounting for management 1.1 Which of the following statements about qualities of good information is false ? A It should be relevant for its purposes B It should be communicated to the right person C It should be completely accurate D It should be timely Answer:C 1.2 The sales manager has prepared a manpower plan to ensure that sales quotas for the forthcoming year are achieved.This is an example of what type of planning? A Strategic planning B Tactical planning C Operational planning D Corporate planning Answer:B 1.3 Which of the following stastements about management acco unting information is/are true? 1 They must be stated in purely monetary terms 2 Limited companies must,by law,perpar management acco unt 3 They serve as a future planning tool and not used as a n historical record

2018年9月acca考试科目变更详情

2018年9月acca考试科目变更详情 在2018年9月的分季考试中,ACCA将迎来一门全新的科目:SBL(Strategic Business Leader)。SBL将原有的P1和P3两门科目合并,在吸收了两门科目大量内容的基础上,从更高视野、更深层次全面提升对于学生整体能力的考察力度。 需要提醒大家的一点是:18年9月考季前已经通过P1和P3考生,将自动转换为已通过SBL;如果只通过其中一门的话,已通过的一门则成绩作废,需要重新进行SBL的考试。 SBL包含了P1和P3的大部分内容,但是SBL更加侧重培养解决实际问题的能力,这也是新科目与之前最大的差异所在。新增添的“职业技能”板块就是为了考验考生在答题中是否能体现出专业能力,这一部分在考试中占有20分的比重,将成为考生们不得不攻克的一个重要环节。 考试建议 1.时间管理 考试全程240分钟,时间紧任务重,官方建议大家运用约40分钟的时间来阅读题目,并大致了解重要信息的位置,以方便答题时快速寻找。 2.高效阅读 整个考试的文本长度大概在12-18页之间,你的整个阅读过程应该为答题要求所驱动,学会提炼重点,提升对知识点考察的敏锐度,这些能力都需要在日常阅读中加以练习。 3.仔细审题 切中题目痛点,准确分析题目要求,如果没有说到点子上,即便表达得再好也很难获得分数。 4.全局规划

纵览试卷全局,有哪些分数有十足的把握,有哪些分数可能需要多下点功夫,在作答前要将这些了熟于胸,掌控好考试节奏,以智取分。 5.写作技巧 下笔前一定要把握好自己的角色定位,将自己完全代入角色,站在角色的立场解决特定的问题。 考试要求 确保你回答的是与题目所要求的相关性最高、最重要、最关键的点,以质取胜切勿以量取胜。注意展现对问题的深度理解力,善于整合场景资源,并提升对所学知识的迁移能力,切勿仅仅照搬原文或者仅陈述原文所呈现的浅显易懂的点。 讲重点,避免答案冗长,陈述过的点不必重复。注意表达的书面性,谨慎对待动词的使用。处理多项答案时,注意各个论点的优先顺序,注意答案呈现的逻辑性以及递进性,切勿“机关枪”一般毫无头绪的简单陈列。 在答题感觉上,始终保持一种“方案即将投入使用”的场景感,始终将利益相关者的需求置于首位。需要记住,SBL考试并非考察语言的雄辩力或者词汇的丰富性或者语法的准确性,它不是一门语言考试,你的专业知识点仍是首要重要的。

ACCA考试模拟试题2

ACCA考试模拟试题2 Required: Prepare a report for the Board of Directors,evaluating the financial and non-financial impact of all the three proposals to Doric Co's main stakeholder groups,that includes: (i)An estimate of the return the debt holders and shareholders would receive in the event that Doric Co ceases trading and is closed down.(3 marks) (ii)An estimate of the income position and the value of Doric Co in the event that the restructuring proposal is selected.State any assumptions made.(8 marks) (iii)An estimate of the amount of additional finance needed and the value of Doric Co if the management buy-out proposal is selected.State any assumptions made.(8 marks) (iv)A discussion of the impact of each proposal on the existing shareholders,the unsecured bond holders,and the executive directors and managers involved in the management buy-out.Suggest which proposal is likely to be selected.(12 marks) Professional marks will be awarded in question 1 for the appropriateness and format of the report.(4 marks) (35 marks) 2 Fubuki Co,an unlisted company based in Megaera,has been manufacturing electrical parts used in mobility vehicles for people with disabilities and the elderly,for many years.These parts are exported to various manufacturers worldwide but at present there are no local manufacturers of mobility vehicles in Megaera.Retailers in Megaera normally import mobility vehicles and sell them at an average price of $4,000 each.Fubuki Co wants to manufacture mobility vehicles locally and believes that it can sell vehicles of equivalent quality locally at a discount of 37.5% to the current average retail price. Although this is a completely new venture for Fubuki Co,it will be in addition to the company's core business.Fubuki Co's directors expect to develop the project for a period of four years and then sell it for $16 million to a private equity firm.Megaera's government has been positive about the venture and has offered Fubuki Co a subsidised loan of up to 80% of the investment funds required,at a rate of 200 basis points below Fubuki Co's borrowing rate.Currently Fubuki Co can borrow at 300 basis points above the five-year government debt yield rate. A feasibility study commissioned by the directors,at a cost of $250,000,has produced the following information. 1.Initial cost of acquiring suitable premises will be $11 million,and plant and machinery used

ACCA各科目学习安排

ACCA各科目学习安排 本文由高顿ACCA整理发布,转载请注明出处 根据ACCA科目的不同类型,我们将ACCA科目分为两大类: 1.文字表达类 2.计算类。 文字表达类: F1, F4, F8, P1, P3 文字类科目的特点在于:记忆为主,思路为主,因此这些科目的学习方法和计算类科目的学习方法略有 差别,除了第一阶段相同以外 第一阶段:8月-9月用20天至30天左右的时间听课,在这个阶段不建议大家去做题,可以去参考讲义以及课本上的小例题,但是不要去做综合题,因为思路尚未建立,很多题目做起来比较困难,会比较浪费时间,因此以听课为主,尽可能将全部课程先听一遍! 第二阶段:9月-10月这个时候你去做题,你会发现思路不清楚,为什么这样答呢?以及读题解题能力比较差,那么这个时候去记忆知识点,去尝试着总结练习册上的题目,列提纲,列要点,不断的加强记忆,因此这个时候建议大家准备一个专门的笔记本,以便我们复习的时候用到. 第三阶段:10月-11月第二遍题目,加强记忆,因为此时你会发现第一遍的记忆已经很模糊,第二遍的思路整理是至关重要的,不断的强化答题要点! 第四阶段:11月-考前,不要用手去写,因为会浪费时间,按照当期重点来进行准备,固定句型,固定答案,固定要点一定要沉着于胸!一定要做到标准化的商业书写,因为考官在这一块的要求是比较高的,而这一块 往往是我们学生做得最不好的地方! acca学习之ACCA各科目学习安排 计算类: F2, F3, F5, F6,F7,F9,P2,P4,P5 计算类科目的特点: 以动手为主,练习为主,所以我们的建议安排如下 第一阶段:8月-9月用20天至30天左右的时间听课,在这个阶段不建议大家去做题,可以去参考讲义以及课本上的小例题,但是不要去做综合题,因为思路尚未建立,很多题目做起来比较困难,会比较浪费时间,因此以听课为主,尽可能将全部课程先听一遍! 第二阶段:9月-10月同学第一遍听课并不能够掌握相关课程的精华,一般只能消化70%左右,但是有了第一遍听课的基础,这个时候大家就要开始来做练习册以及真题的题目了,我们一般建议学生练习册要至少做三遍,那么这就是第一遍,以掌握知识为主,第一遍做题的时候可以参考答案做对知识以及解题思路的 梳理!而这个时候同学可以选择再听一听老师的网校课程,加深思路

相关文档

- ACCA各科目学习安排

- acca考试科目

- ACCA的考试科目顺序

- 对于ACCA考试科目中F8的题型分析

- ACCA考试科目F1-F4考试题型及考试重点

- ACCA考试科目(AFM)中的考试易错点总结

- 2017年ACCA考试科目F6税法知识点总结

- 2019ACCA考试科目 F5备考攻略

- 2018年ACCA F5-F5考试各科目题量及分值

- 2018年9月acca考试科目变更详情

- 2019年ACCA考试科目介绍,包含SBL改革说明

- acca考试科目

- ACCA考试审计科目模拟测试(4)

- ACCA各科目全球最高分一览表

- acca考试科目

- ACCA考试科目内容完整介绍从F1到F7

- 2019年ACCA考试科目F6易忘知识点归纳(下)

- 最新最全ACCA中F5大纲考试科目介绍

- 2018ACCA考试时间和科目

- ACCA F阶段与P阶段共14门科目简介